News

Spring forecast: Ukraine war significantly burdens German economy, inflation at record high

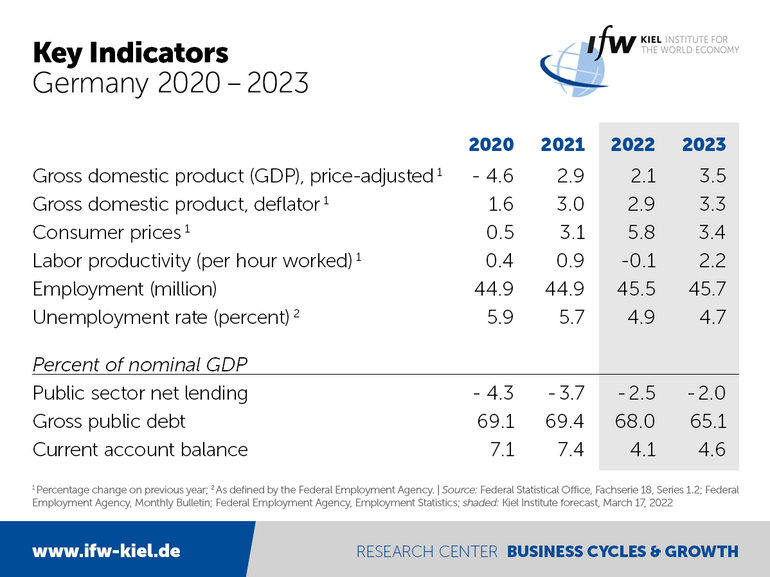

The Ukraine shock delays the return to pre-COVID-19 levels into the second half of the year. Production capacity will remain underutilized until the end of the year and economic output will therefore remain below potential. In the coming year some of the production losses will be made up for and the economy should then grow by 3.5 percent (previously 3.3 percent expected). The economic turmoil caused by the war in Ukraine is likely to costGermany a total of around 90 billion euros in economic output this year and next in total.

"Without the strong post-pandemic boost, German economic output would be down this year. The economy in Germany and worldwide is subject to opposing forces. The strong upward and catch-up effects following the removal of most infection control measures are offset by the shock waves resulting from the Ukraine war," said Stefan Kooths, head of the economic forecast and vice president of the Kiel Institute for the World Economy, on the occasion of the spring forecasts for Germany, the euro area, and the world economy presented today.

In the euro zone, GDP is expected to increase by 2.8 percent (2022) and 3.1 percent (2023). The global economy is expanding at a much slower rate than would have been expected without the war.However, at rates of 3.5 percent this year and 3.6 percent next year, it is still expected to grow somewhat faster than the longer-term trend. The Russian economy will slip into a severe recession.

The war in Ukraine is impacting the economy through greater uncertainty, new stress in supply chains and further increases in raw material prices, especially for oil and gas. Overall, Germany's energy import bill in 2022 is likely to be around 40 billion euros higher than estimated in the December forecast.

However, consumers in Germany have accumulated additional savings of 220 billion euros during the pandemic phase. Furthermore, industrial companies are sitting on record high order backlogs of 100 billion euros, around 17 percent of their annual production. These special factors cushion the Ukraine shock, so that although the economic recovery after the COVID-19 pandemic is severely impacted in the short term, it is not interrupted.

Record inflation in reunified Germany and the euro area

The sharp rise in prices for imported raw materials and intermediate inputs has not yet fully reached consumers. Significant, broad-based inflationary pressure had already built up before the Ukraine war, and this will be reflected in high inflation rates throughout the year, even if—as assumed in the forecast—commodity prices ease again somewhat and supply bottlenecks gradually ease in the second half of the year.

At an average of 5.8 percent for the year, inflation is expected to be higher than ever before in reunified Germany. In 2023 inflation is likely to be 3.4 percent. In the construction industry in particular, prices are rising dramatically, by 8.6 percent last year—by far the highest price increase since reunification. It is likely to be even higher this year before moderate again next year.

At 5.2 percent, the inflation rate in the euro zone is likely to reach its highest level since the establishment of monetary union. At 2.8 percent, the inflation rate is also likely to clearly exceed the inflation target of the European Central Bank (ECB) in2023.

"Inflationary pressures are also due to the expansionary monetary and fiscal policies pursued worldwide during the pandemic. The massive financial aid—largely financed by central banks—created phantom incomes on a large scale in the private sector, this means incomes which were not matched by production and which therefore have an inflationary effect. Inflation gets a further boost by the war, but it was already underway long before the invasion of Ukraine," says Kooths.

Debt rises, labor market remains robust

Employment is continuing its recovery from the COVID-19 crisis, although the pace is slower. The number of people employed will rise from 45.5 million this year to 45.7 million next year. The economic consequences of the Ukraine war will have a dampening effect. Plus, the increase in the minimum wage to 12 euros will lead to employment losses (see IfW Kiel media information (German only): Minimum wage of 12 euros: Risks for employment increase, poverty hardly decreases). Labor supply will reach its peak next year due to the aging of society. Unemployment will fall from 5.7 percent (2021) to new all-German lows of 4.9 percent (2022) and 4.7 percent (2023).

Although public-sector debt is declining following the COVID-19 pandemic, it remains high. In the form of special funds for climate protection and defense, the federal government has created the preconditions for financing deficits on a larger scale to be possible despite the debt brake. In 2022, the deficit will be 92 billion euros, and in 2023, when the debt brake is to take effect again, it will be a good 81 billion euros. Germany's public debt will then amount to 68 percent (2022) and a good 65 percent (2023) of gross domestic product (GDP).

"Germany's list of unresolved distribution conflicts is getting longer and longer. Unfunded benefit promises in the pension and healthcare systems, ambitious climate protection measures, more defense spending, cushioning high energy prices—so far, fiscal policy has always swerved into new debt. It is not debt sustainability that is the problem, but the fact that this fiscal stance fits less and less into the overall economic landscape, not least because it gives fuels inflation pressure. In times of demographically dwindling growth forces, it is necessary to adjust demand to production capacities. This requires budget consolidation, ideally by prioritizing spending," says Kooths.