News

EU Financial Transaction Tax: Instrument suitable, proposed implementation flawed

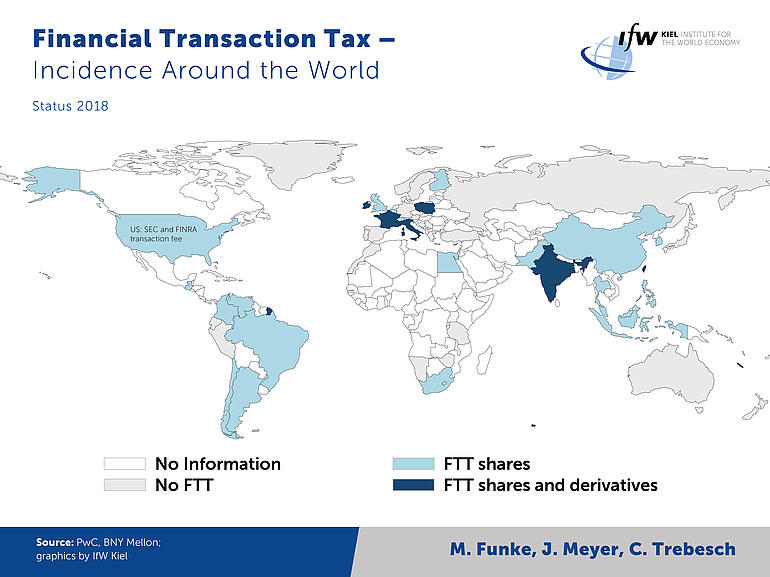

“A tax on stock trading is internationally and historically the rule rather than the exception. Half of the G20 countries impose such a tax. However, the design of the tax is crucial. The current concept for an EU financial transaction tax (FTT) is rightly being criticized, among other things because it refrains from taxing derivatives and OTC trading,” said Christoph Trebesch, Head of the Research Centre International Financial Markets and Global Governance at the Kiel Institute for the World Economy. He was in charge of the recently published report “The German-French Proposal for an EU Financial Transaction Tax” (Manuel Funke, Josefin Meyer, Christoph Trebesch 2020) commissioned by the Federal Ministry for Economic Cooperation and Development.

Proposal has strengths

From an economic point of view, a well-designed FTT can be supported in principle, provided that the tax rate is low and the avoidance effects are limited. The report emphasizes that the planned tax rate of 0.2 percent is moderate and comparable to the international average. Studies show that with such a rate, market distortions and tax evasion tendencies are likely to be limited. The tax collection costs would also be low, probably at 0.1 to 0.2 percent of revenue. Examples from other countries show that the tax can be levied effectively via a few central clearing houses. The proposal is generally based on functioning models such as those used in large financial centers such as Switzerland, the UK, Singapore, or Hong Kong.

German “small investors” not the main target

According to the study, German private households would only pay a small proportion of tax revenues. “A large part of the tax revenue in Germany would be raised from foreign professional investors, since they hold and trade most DAX shares,” said Trebesch. Estimates show that in 2018 only about 15 percent of DAX stocks were held by German households, while US pension funds and foreign sovereign wealth funds are becoming increasingly important.

Restriction to exchange-traded shares is a mistake

According to the report, the main weakness of the proposal is its limitation to stock exchange trading. Derivatives are excluded, even though they account for over 80 percent of financial transactions in Germany and the euro zone. An isolated share tax can therefore not be justified from an economic and financial point of view.

“The planned exceptions create undesirable incentives in favor of unregulated markets and financial products and discriminate against all those who rely on traditional stock trading,” Trebesch said. The inclusions of derivatives and over-the-counter trading would double tax revenues, conservatively estimated.

“In order to avoid distortion effects and loss of income, it is essential to learn from the experience of the FTTs in Italy, Sweden, or France,” said Trebesch. These showed that a broader tax base reduces avoidance strategies.

The researchers at Kiel Institute therefore propose extending the FTT to over-the-counter (OTC) trading and derivatives, albeit at a significantly lower tax rate of 0.01 to 0.02 percent, as turnover rates in the derivatives market are extremely high. In addition, the tax should be extended to bond transactions and high frequency trading.

A centralized electronic clearing system such as that in the UK is particularly recommended. If possible, the rules should be clear from the first day of introduction and should contain few exceptions.