Kiel Institute Highlights

Germany will remain attractive for Chinese investors - Covid-19 won´t stop the trend

Germany is one of the most important target countries for Chinese investors and ranks tenth worldwide in terms of Chinese foreign direct investment stock abroad. The German transport sector and technology sector in particular have received a huge amount of investment from Chinese investors in recent years. This indicates that investing in Germany remains strategically important for Chinese investors seeking access to key technologies. Overall, the COVID-19 pandemic had little and, above all, only a short-term negative impact on Germany’s attractiveness for Chinese investments.

The German transport and technology sectors are the main target industries of Chinese investors.

China is now the third largest investing country worldwide. While many Chinese companies investing abroad are initially motivated by their own business objectives, the Chinese government and its industrial and economic policies also play an important role in directing and regulating such overseas investment. Germany is now clearly an attractive destination for Chinese outward foreign direct investment (OFDI). Crucial to this has been the Chinese government’s paradigm shift away from low-tech, labor-intensive manufacturing activities toward innovation-driven economic growth and higher value-added production activities.

Against this backdrop, we took a closer look at the development of China’s investment in Germany over time based on four datasets, including our own survey,which helps explore the role of the COVID-19 pandemic in this regard in 2020–2021. There are four main findings from the analysis (Xia and Liu, 2021):

Firstly, Germany’s attractiveness for Chinese investment increased over time. In 2019, Germany was ranked tenth among all target countries for Chinese investment (in stock). Chinese investors substantially increased their investment flows to Germany after the global financial crisis. At that time, China shifted toward encouraging quality- and innovation-based economic growth, with OFDI being an important instrument for Chinese firms to better access know-how and advanced technologies from abroad. From 2009 to 2017, Chinese OFDI flows to Germany increased steadily (with 2015 being an exception) at a much higher rate than Chinese OFDI in general.

With the Chinese government strengthening its guiding role and regulatory power with regard to Chinese overseas investment projects in 2017, there was a substantial reduction in Chinese investment flows to Germany in 2018. However, they remained stable in 2019 against the backdrop of further decreasing Chinese overseas investment in general.

Secondly, Chinese state-owned enterprises (SOEs) play an important role as investors in Germany—particularly with regard to large-scale investment projects with transaction values of at least USD 100 million. From 2011 to 2014, Chinese SOEs accounted for a significantly larger share of Chinese firms’ “large-scale” investment transactions in Germany than in the case of Chinese FDI projects in Germany in general. More recently, when the Chinese government again tightened its investment regulations, the number of large-scale projects in Germany involving Chinese SOEs decreased sharply from 2016 to 2017 but remained constant after that. The number of large-scale projects by non-SOEs decreased more sharply in the same period. The average size of SOEs’ large-scale investment transactions was also larger than that of their non-SOE counterparts in almost all years from 2011 to 2019.

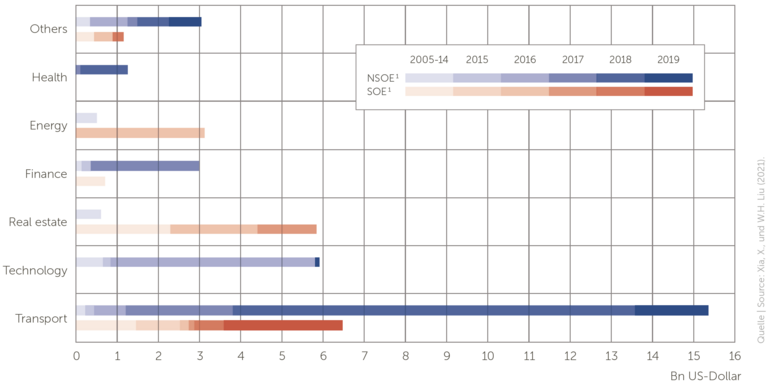

Transaction value of Chinese large-scale investment projects in Germany (at least USD 100 million, by target industry and by investing firm ownership)

1 SOE for state owned enterprises und NSOE for non-state owned enterprises. Note: The sectoral classification from AEI & HF (2020) is different from the UN’s International Standard Industrial Classification.

Thirdly, in terms of large-scale investment projects, the German transport sector and technology sector have been the main industries targeted by Chinese investors in the recent past. Almost USD 22 billion flowed into the transport sector over the 15 years to 2019, nearly USD 6.5 billion of which came from SOEs. Over 90 percent of the money was invested in the last five years, i.e., after the announcement of the Made in China Strategy 2025 in 2015. Nearly USD 6 billion flowed into the technology sector, predominantly through investment projects by non-SOEs— here again, nearly 90 percent of the total was invested between 2015 and 2019. The third sector favored by Chinese investors for large-scale investment projects in Germany was real estate. A total of USD 6.5 billion was invested in this sector between 2005 and 2019, USD 5.8 billion of which came from SOEs. Unlike investment in the transport and technology sectors, investment in the real estate sector has declined in the recent past (see figure).

Fourthly, the COVID-19 pandemic had some negative, but rather limited, impacts on Germany’s attractiveness for Chinese investments. Our own survey in the summer of 2020, which covered consulting firms and organizations in Germany that proviFDI consulting services to Chinese investors, shows that a majority of them received fewer general enquiries from Chinese investors regarding investment in Germany in the first half of 2020 than in the same period of 2019. Our findings also suggest that although Chinese investors appear to be more cautious about initiating new investment projects in Germany due to the pandemic, many of them did not immediately choose divestment or a market exit. Business registration services were thus also less in demand from Chinese investors in this period, while more enquiries for consulting services around employment and labor issues, financing, liquidity problems, and supply chain disruption between the EU and China were observed. China is aiming to further increase its technological innovation capabilities in order to achieve high-quality economic development. In doing so, it needs access to knowledge and technologies from abroad, including from Germany. Germany’s importance as a destination country for Chinese investment will therefore grow further in the future. This raises some critical questions that deserve more attention from policy makers. For example, how can Germany deal with planned Chinese investment where the Chinese government plays a strong guiding role? How can national security concerns best be addressed without unduly curbing Chinese investment? How can fair competition, espe cially with regard to mergers and acquisitions, be better ensured? How can German firms and industries facing more intense competition (from China) boost their competitiveness and how can the German government provide support in this regard?

Related Publication

References:

Xia, X., und W.-H. Liu (2021). China’s Investments in Germany and the Impact of the COVID-19 Pandemic. Intereconomics, 56 (2): 113–119. DOI: 10.1007/s10272-021-0962-0.