News

Sovereign debt in Africa: large interest rate differences across creditors

"Since many countries borrow money from multiple creditors at the same time, this means that taxpayer funded institutions may end up subsidizing the financial returns of both private bondholders and Chinese banks," says Christoph Trebesch, research director and debt researcher at Kiel Institute.

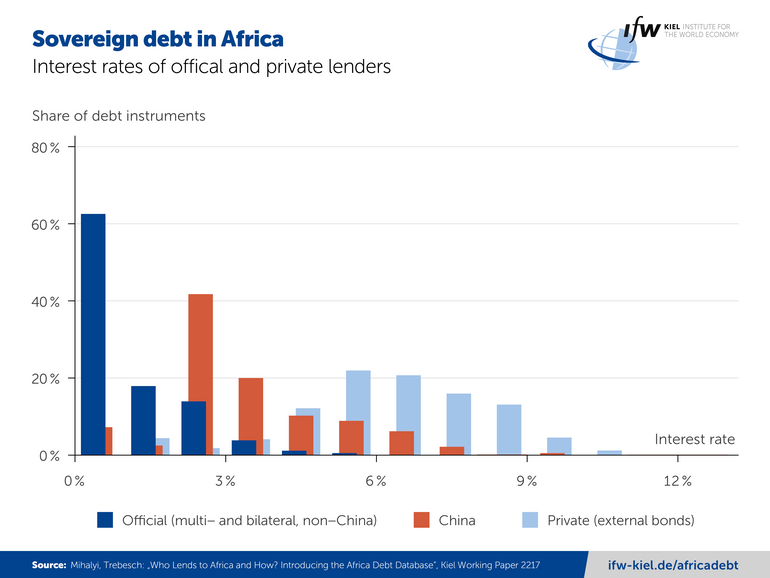

Private bondholders, mostly investment and hedge funds, receive coupons of up to 10 percent from African states. On average private external bonds carry interest rates of 6.2 percent.

By contrast, loans by international public institutions like the World Bank, carry a much lower average interest rate, of only around 1 percent. Loans from bilateral, government lenders tend to have somewhat higher interest rates, with Germany and France charging average rates of 1.7 percent, while loans from Japan are the cheapest at an average of 0.5 percent.

China plays a special role as a creditor. Although the loans are also granted by the state or through state-owned banks, Beijing charges on average 3.2 percent interest rates and therefore significantly more than the other state creditors.

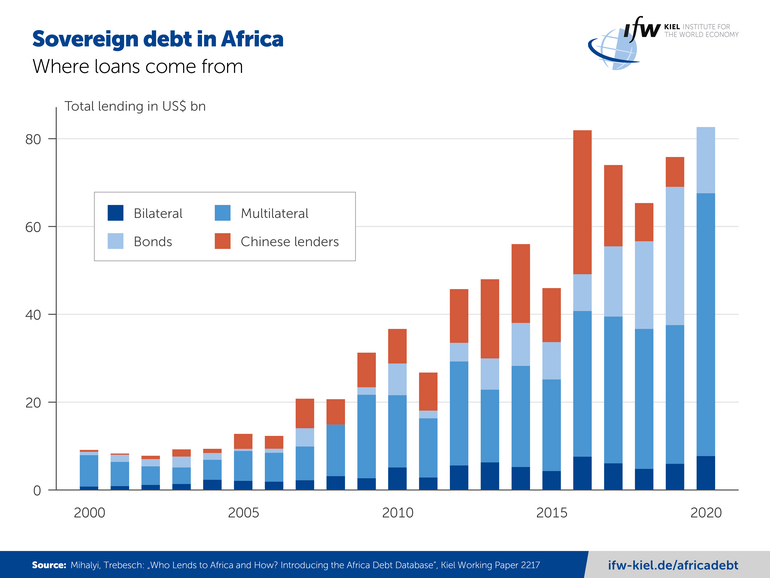

The analysis is based on the new and freely accessible Africa Debt Database (Who Lends to Africa and How? Introducing the Africa Debt Database) of the Kiel Institute for the World Economy. It contains more than 7,400 loans and bonds from over 50 different public and private external lenders between the years 2000 and 2020 with a total volume of USD 790 billion .

So far, data on African sovereign debt have been mainly accessible in aggregate form, i.e., with information on average interest rates vis-à-vis all creditors. However, information on the terms of individual contracts and individual creditors was often missing or incomplete.

"A key objective of the Africa Debt Database is to increase the transparency of Africa's sovereign debt. Individual debt instruments have enormously high interest rates, while many others have little or no interest costs. We were surprised to see how big the differences really are across different creditors and this was unrecognizable in the data available to date," says Trebesch.

Private investors from the West and Chinese banks benefit from subsidized development loans

The interest rate gap across creditors to African states has widened significantly over the past 20 years. In the 2000s, the interest gap between loans by state-owned lenders and debt raised from foreign bondholders averaged only 0.5 to 1 percentage points, but in recent years it has been around 5 percentage points. The reason is that the coupon on African bonds in the international capital market rose significantly, while public lenders now charge even lower interest rates than they did then.

"The interest burden on private bonds has risen significantly in recent years and is putting increasing pressure on the national budgets of poorer African countries in particular. It is not so much the difference in interest rates that is remarkable, because public lenders often have a political mandate and the goal of helping African countries to develop. In contrast, private investors focus on financial returns," says Trebesch.

"What is more worrying is that numerous countries, such as Egypt or Kenya, are simultaneously borrowing money both from private investors and, on a large scale, from public lenders, so that the low-cost loans from the public sector—ultimately taxpayers' money—are being used to cross-finance the high returns of private investors such as hedge funds. The same is true of Chinese loans from African countries, some of which are serviced with the help of cheap development loans from Western countries."

Huge capital needs in an emerging Africa

In the last 20 years, African countries have recorded very high growth rates, on average, and the demand for capital has strongly increased too, for example to finance the construction of basic infrastructure. Yearly sovereign debt issuance has risen from around USD 10 billion in the early 2000s to around USD 80 billion between 2016 and 2020.

Government bonds issued on the international capital market and Chinese loans played only a minor role in the 2000s, but were then largely responsible for the African borrowing boom from 2008 onward. In some years, these two creditor groups account for a quarter or almost half of African sovereign borrowing.

"Our micro data enable a systematic reassessment of sovereign debt in Africa. We can now better answer key questions like: who is lending money to African governments and on what terms? The new, publicly available and detailed data makes analyses of debt sustainability and sovereign default risk in Africa easier to conduct," Trebesch said. "Given the growing debt difficulties on the continent, more analysis on the characteristics and composition of Africa’s sovereign debt is crucial."