News

Kiel Institute winter forecast: Economic Outlook for 2022 significantly worsened

"Overall, the dent in the recovery process caused by the ongoing wave of infections is somewhat larger than we had expected in our autumn forecast. However, thanks to progress in vaccination, the setback will be nowhere near as severe as in the previous winter half-year. The economic consequences of the pandemic are still sensitive, but they are decreasing from wave to wave," said Stefan Kooths, the Kiel Institute’s vice president and research director business cycles and growth, on the occasion of today's publication of the economic outlook for Germany (German Economy: Recovery temporarily on hold) and the world economy (World Economy: Transitory slowdown).

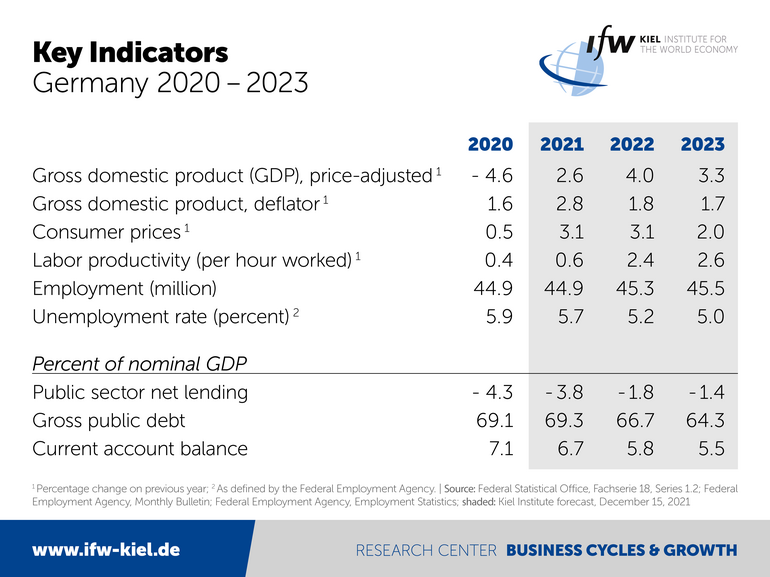

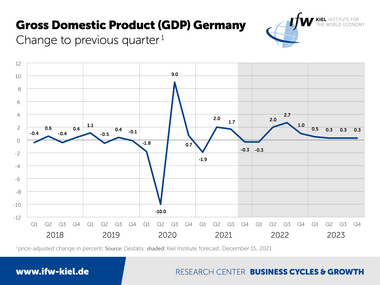

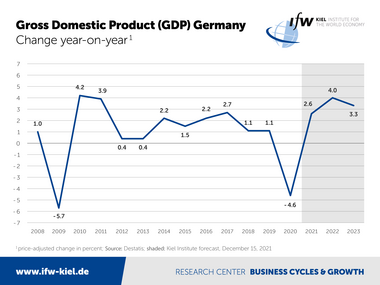

GDP is expected to contract by 0.3 percent in each of the two quarters of the winter half-year before the upswing picks up again strongly from spring 2022 onwards, when the burdens of the pandemic ease. Additional momentum will come from the fact that supply bottlenecks, which are currently weighing heavily on industrial production, should gradually be overcome.

The pre-crisis level of GDP will not be reached until the 2nd quarter of 2022. Macroeconomic production capacities will probably not be normally utilized again until the third quarter of 2022. Until then, the delayed recovery because of the more severe fourth Covid-19 wave will cost economic output of around EUR 40 billion, with consumer-related service sectors being particularly affected.

Inflationary environment in the wake of the pandemic

Inflation will remain high for the time being, and the inflation rate is likely to be 3.1 percent both this year and next. This is due on the one hand to supply bottlenecks, which continue to increase manufacturing costs and tighten the supply of consumer goods. At the same time, private households have accumulated additional savings of around EUR 200 billion increasing their willingness to pay. In 2023, inflation is likely to be 2 percent.

Construction prices are rising particularly strongly. They are likely to rise by almost 8 percent this year, around 2 percentage points more than in 1992 during the reunification boom. Price increases are also likely to be strong in the next two years, with rates of a good 5 and a good 3 percent respectively.

Budget deficit also in 2023: Ampel coalition creates more fiscal space

Public budgets remain well in deficit until the forecast horizon, even though revenues are bubbling up strongly and tax receipts have already exceeded their pre-crisis level. The deficit falls from 3.8 percent of GDP this year to 1.8 percent in 2022 as the burden of the pandemic eases.

The budgets are expected to close with a significant deficit of 1.4 percent in 2023. The size of the deficit would violate the previous debt break. For this reason, the Ampel coalition changes the rule in such a way that loans originally approved for anti-pandemic purposes but not drawn down can be used later via the Energy and Climate Fund.

"The fiscal stance does not fit the macroeconomic landscape for the next few years. The recovery from the Covid-19 crisis is not sputtering for lack of demand. The buoyant forces—high pent-up purchasing power among private households, record order backlog in industry—remain intact. They are more than sufficient to bring production back to normal capacity utilization. There is no need for further stimulus programs as the economy risks diving into post-pandemic overheating. Demographics causes potential growth to weaken significantly and decarbonization is putting an additional strain on production capacity. Thus, prioritizing government spending rather than deficit boosting is the way to go for," says Kooths.

The recovery on the labor market will be interrupted by the fourth wave, and a substantial part of the work shortfall is likely to be absorbed by short-time working schemes once again. After a period of stagnation in the winter half-year, the number of employed people will initially pick up again. The increase in the minimum wage to EUR 12, which is expected to take effect on July 1 next year, will have dampen the job market recovery. In 2023, with 45.5 million people employed, the peak in employment will be reached. The unemployment rate will fall from 5.7 percent (2021) to 5.2 percent (2022) and 5.0 percent (2023).

Germany's much-criticized current account surplus falls to 5.8 and 5.5 percent of economic output in the next two years. The decline is largely due to the fact that import prices are rising much faster than export prices.

Biontech adds another 0.5 percent to 2021 GDP

In the final accounts for 2021, royalty revenues from vaccine developer Biontech due towards the end of the year from its US manufacturing partner Pfizer is expected to increase GDP growth by almost 0.5 percentage points from 2.6 to around 3 percent. This effect has not been included in the forecast's table of figures, as—following the accrual principle—the total amount will also affect past quarters that are expected to be revised in the official national accounts.

Recovery of the global economy has lost momentum

"Renewed increases in Covid-19 infections are slowing economic activity also outside Germany, supply bottlenecks have hampered the upturn in global industrial production, and the Chinese economy appears to be out of step," Kooths said. For 2021, the Kiel Institute expects global output to grow by 5.7 percent (previously 5.9), and by 4.5 percent in 2022 (previously 5.0). For 2023, the outlook has improved slightly to 4.0 percent (previously 3.8).

Considerable upside and downside risks for the winter forecasts stem from the further course of the pandemic—not least with regard to the Omikron variant—as well as from the time it takes to overcome supply bottlenecks. The Kiel Institute expects both effects to continue to noticeably dampen economic activity in the coming months. Covid19-related restrictions are expected to end from next spring onwards, while supply bottlenecks are unlikely to be completely overcome before the end of 2022. In addition, this forecast can only partially reflect the economic and financial program of the new federal government, as this has yet to take shape in concrete legislative decisions