News

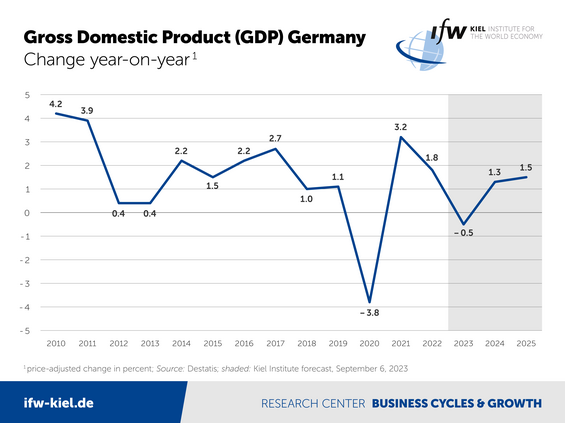

German economy to shrink by 0.5 percent in 2023

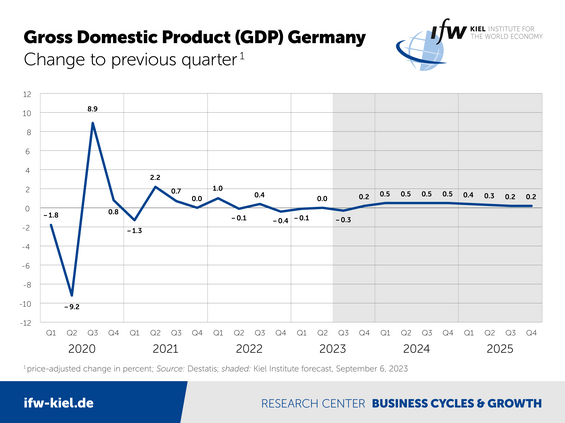

Although negative factors such as the high level of sick leave and supply bottlenecks have eased, gross domestic product (GDP) has not yet returned to an expansionary course. The economy is not expected to pick up speed again until the turn of the year.

"Germany is now feeling the effects of its old industrial business model. In addition, the interest rate turnaround is weighing on the economy at home and via export markets. Central banks have successfully shown their teeth in the fight against inflation and the German economy must now hold its own with these headwinds," says Moritz Schularick, President of the Kiel Institute.

"Overall economic activity is currently weak and stagnating, but capacity utilization rates will recover over the projection period. However, economic output will then be around 3 percent below the level that was projected for 2024 and 2025 prior to the pandemic. The German economy hits its production limits more quickly in the future, so greater attention should be paid to measures to boost potential," says Stefan Kooths, head of forecasting at the Kiel Institute, on the occasion of the economic forecasts published today for Germany, the euro area, and the world. All three reports can be found in our subject dossier Economic Outlook

A weak manufacturing and construction sector are weighing on the German economy. Some segments of energy-intensive production are no longer profitable and are unlikely to become so again. Exports are suffering from the global weakness in investment. However, the still high order backlog is supporting industrial activity.

In addition to China—where economic momentum has recently fallen short of expectations and is likely to remain subdued due to structural problems—other important advanced economies such as South Korea are also in weak shape. However, the still high order backlog is providing support for German production.

In the construction sector, considerably more expensive financing sends residential investment in particular further downhill, the sector is expected to shrink by almost 3 percent in the current year and by almost 4 percent in the coming year. Only in 2025, after four negative years in succession, is there likely to be an upturn—but then starting from a level that is lower than it has been for eight years.

"Current construction and inventory prices no longer match financing costs after the turnaround in interest rates. Without significant price corrections, the construction industry will hardly get going again, and there is scope for this," says Kooths.

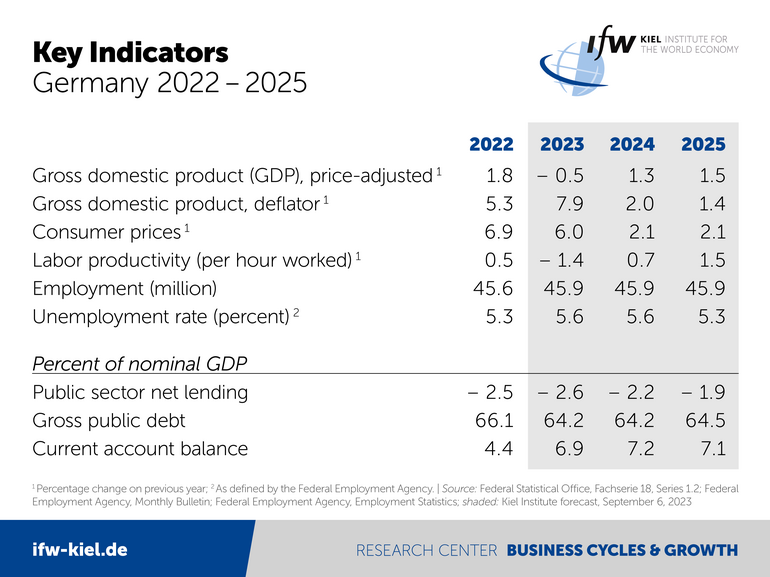

Consumer spending is expected to fall slightly by 0.6 percent in 2023, but to grow strongly by 2 percent next year as a result of higher wages and expanded government transfers, thus stimulating the economy and consumer-related industries. Mass purchasing power will then increase by 3.3 percent (2024) and 2 percent (2025).

Inflation rate falls to 2 percent, core rate remains significantly higher

According to the forecast, inflation in Germany will fall significantly because the general upward trend in prices is weakening and energy prices continue to fall, albeit not to pre-crisis levels. After 6 percent this year, inflation will be around 2 percent in the next two years.

However, the core rate adjusted for energy prices is likely to remain well above 2 percent in 2024 and 2025, as services in particular will only follow the general surge in inflation with a time lag.

The current phase of economic weakness will leave little mark on the labor market, as the shortage of skilled workers remains high. As a result, the unemployment rate willfall from 5.6 percent in this and the next year to 5.3 percent (2025).

In the wake of demographic change, employment will pass its peak next year and is expected to decrease to around 45.8 million by the end of 2025.

Despite the economic recovery, the government's budget deficit declines only slightly—from 2.6 percent as a share of GDP in the current year to 1.9 percent in 2025. The debt ratio remains at around 64 percent as a share of GDP over the entire period.

As the international environment gradually brightens, external tradeis likely to gradually pick up again. Following a decline of 1.3 percent (2023), exports will initially move sideways at plus 0.5 percent (2024). In 2025, they will once again become a more important growth driver, rising by 3.6 percent in a generally stronger global economic environment.

Global economy and euro area: US economy surprisingly robust

In the United States, the economy is proving surprisingly robust in view of the massive rise in interest rates. Overall, the global economy will expand at a moderate pace over the forecast period and is expected to grow by 3.0 percent this year and by 2.8 and 3.2 percent respectively in the next two years.

In the euro area, economic momentum remains subdued, with GDP expected to increase by 0.6 percent in the current year, followed by growth of 1.4 percent (2024) and 1.7 percent (2025).