News

Kiel Institute Economic Outlook: Germany on the Brink of Recession

The German economic outlook has been adversely affected above all by the political uncertainty caused by trade conflicts and the Brexit crisis, with investment and exports coming under particular pressure. In addition, there are cyclical factors due to the previous long upswing. In the third quarter of 2019, gross domestic product (GDP) is expected to shrink by 0.3 percent, following a slim decline of 0.1 percent in the second quarter. "Germany thus formally meets the definition of a ‘technical recession’, but this is not yet associated with a macroeconomic underutilization of capacities. Only in such a case could we speak of a recession in the sense of a cyclical phenomenon," said Stefan Kooths, Head of the Forecasting Centre at the Kiel Institute for the World Economy, on the occasion of today's economic forecasts for Germany, the Euro zone and the world.

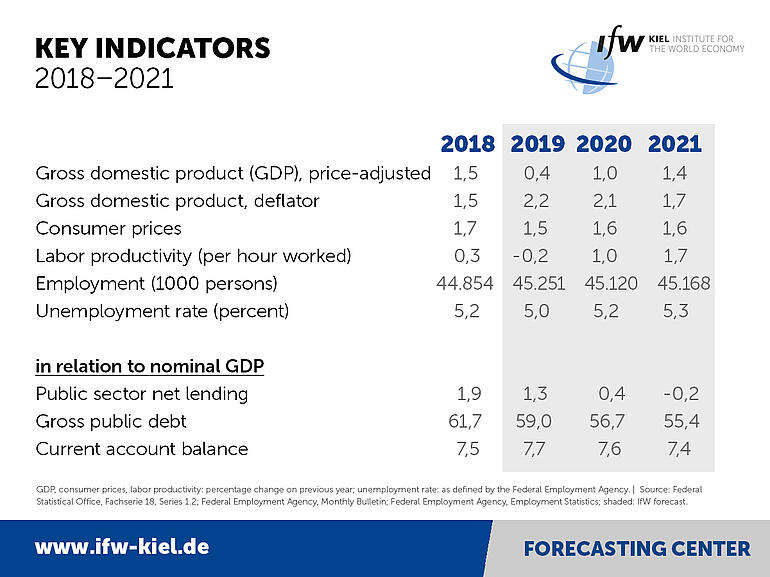

"Based on recently revised national accounts data, the German economy has started cooling down already since the turn of the year 2017/2018, about half a year earlier than previously suggested by the data. For 2020, the researchers now expect GDP to grow by 1 percent (previously 1.6 percent), with almost half of the increase, 0.4 percentage points, being due to the above average number of working days. In 2021.GDP is expected to grow by 1.4 percent.

"The real problem with Donald Trump's trade disputes is not the tariffs themselves, but the great uncertainty about what is to come. Uncertainty is poison for investment decisions," said Kiel Institute President Gabriel Felbermayr. "But many emerging countries around the world still have a lot of catching up to do. This offers very great export opportunities for German mechanical engineers and car manufacturers. There is therefore no reason to question the export orientation of the German economy."

Industry weak, private consumption strong, deficit in national budget expected

While industry has already crossed the threshold of recession, the downturn has not yet fully hit consumer-related service providers and the construction industry continues to run at high speed. "However, the problems in industry will increasingly have an impact on the other sectors, and the recent strong rise in wages makes job cuts more likely during the downturn," said Kooths. "Nevertheless, there is no reason for policy actionism, for example through investment programmes that would above all fuel construction prices. Instead, the national budget should be allowed to breathe with the economy, as provided for by the debt brake. The black zero, however, does not have to be held on desperately."

After 3.6 per cent in the previous year, corporate investment will only increase by 1.4 per cent in the current year and even fall slightly in 2020 followed by a moderate recovery of 2 percent in 2021. Exports are expected to grow by just under 1 percent in 2019, up from more than 2 percent in the previous year, but then to grow somewhat more strongly again at 1.8 percent (2020) and 2.6 percent (2021).

The weaker economy is also making itself felt on the labor market, where the longest upswing in 50 years is coming to an end. The number of unemployed is likely to rise again from now on and the unemployment rate will rise from currently 5 percent to 5.2 percent (2020) and 5.3 percent (2021). In the coming year, the number of people in employment is likely to fall again for the first time since the Great Recession, to 45,120 million.

Nevertheless, the disposable incomes of private households are likely to remain clearly on an upward trend, albeit at a slower pace than before, not least because the shortage of skilled workers will continue to lead to quite strong increases in effective wages of 3.2 percent (2019), 2.4 percent (2020) and 2.8 percent (2021) and numerous fiscal measures such as the partial abolition of the solidarity surcharge will support incomes. In addition, inflation is expected to remain moderate at rates of 1.5 percent (2019) and 1.6 percent (2020 and 2011) and thus not burden the purchasing power of disposable incomes.

Accordingly, private consumption continues to be a pillar of the economy and is likely to grow at rates of 1.3 percent (2019), 1.2 percent (2020) and 1.4 percent (2021). Construction is also likely to remain on an upward trend, rising by 3.2 per cent (2019), 1.7 per cent (2020) and 2.2 per cent (2021), not least due to the continuing extremely favorable financing conditions.

The weakening economy also affects the national budget. Annual surpluses will fall from 43 billion euros this year to 14 billion euros next year and in 2021 will turn into a deficit for the first time since 2011 of 7 billion euros, 0.2 percent of GDP.

Euro zone and global economy: monetary policy revived, political uncertainty dampened

The economy in the euro zone and worldwide is being stimulated in particular by a foreseeable further easing of monetary policy, but the political uncertainty resulting from trade conflicts and populist governments is weighing on the outlook. Industry in particular is in a downturn. GDP in the euro zone is expected to grow by 1.2 percent in both the current and the coming year, and by 1.5 percent in 2021. Unemployment is likely to fall further and fall below its historical low of before the financial crisis.

Since the beginning of the year, global trade has even tended to decline. In the advanced economies, the economy weakened recently, whereas in the emerging markets it picked up somewhat. In the current year, global production is likely to increase by only 3.1 percent, next year by 3.2 percent, after 3.7 percent last year.

"The forecast uncertainty is particularly great due to the current trade policy tensions. We assume that the trade conflicts will not escalate any further and that German exports will gradually pick up speed again. A more rapid easing of the situation would result in a better economic development than predicted, and a renewed escalation of the conflicts would result in a worse economic development. The situation is similar with the still unresolved Brexit process, although the significance for German foreign trade is less than that of global trade conflicts," Kooths said.