News

Kiel Institute Economic Outlook: Exporting manufacturers strengthen German economy

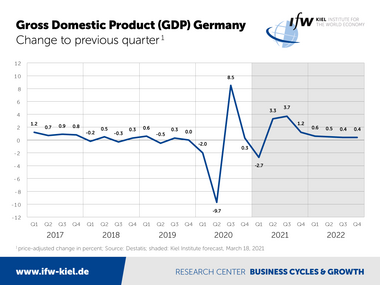

For the first quarter, the Kiel Institute expects economic output to fall by 2.7 percent, as business in consumer services has largely ground to a halt because of stricter social distancing since November. An even stronger setback has been prevented by the manufacturing sector, that benefits from the ongoing global recovery.

"The German economy has clearly spread out over the winter months: While manufacturers continue to make up ground and are hardly held back by the second covid-19 wave, contact-intensive service providers were sent back to the starting blocks," said Kiel Institute’s head of forecasting Stefan Kooths. "Two patterns overlap: In line with its export orientation, output in manufacturing follows a V-shaped course, in contrast, the pandemic marks a striking W on the activity level of the consumer-oriented service sectors."

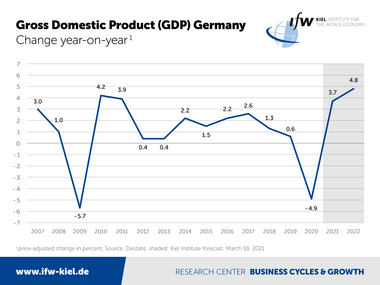

The Kiel Institute’s economic outlook builds on the expectation that, due to a successful vaccination campaign, the economy will recover on a broad front in the course of the summer months. In the second and third quarters, gross domestic product (GDP) is expected to increase at rates of between 3 and 4 percent, so that the pre-crisis level will be exceeded even before the final quarter.

The once again drastic slump in private consumption during the most recent winter semester will be offset by massive catch-up effects in the second half of the year. Private households are accumulating purchasing power of 230 billion euros during the pandemic, due to a lack of consumption opportunities while automatic stabilizers such as short-time working allowances and extra transfers such as the child bonus stabilize private incomes. Exports have been expanding uninterruptedly since mid-2020 and, with thanks to the ongoing recovery of the global economy, are expected to grow strongly by 12.8 percent this year and by a further 5.6 percent next year.

"Once again, the importance of international trade for German prosperity is evident. Foreign business is currently preventing a more severe economic slump and will play a decisive role in the recovery in the current year. Trade restrictions on the part of the EU, for example against the export of vaccines, put a strain on global supply-chains and undermine the German business model," said Kiel Institute President Gabriel Felbermayr.

Pandemic costs 340 billion euros in value-added

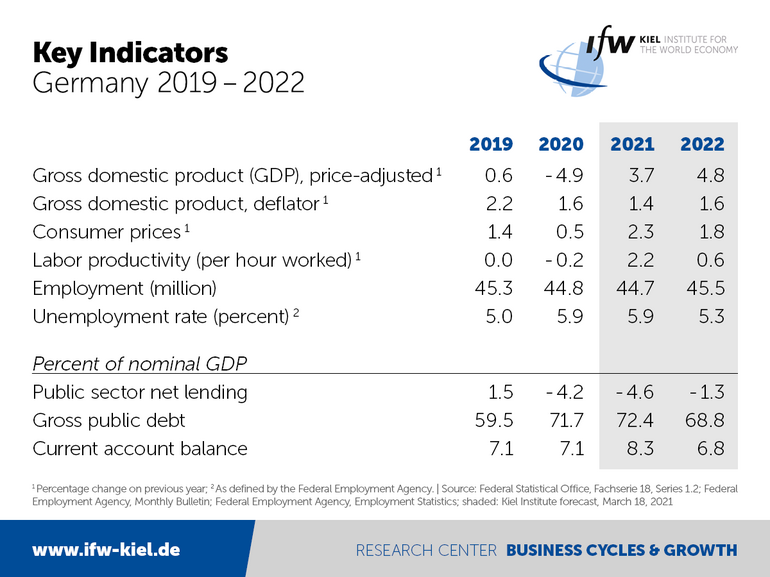

By topping the pre-crisis level of economic activity, the consequences of the pandemic are far from being over. Economic output at the end of this year is estimated to be 1.4 percent below the level to be expected without the pandemic. According to Kiel Institute estimations, the pandemic-related loss of value-added amounts to 340 billion euros for the period of 2020 to 2022.

Unemployment will remain comparatively low at rates of 5.9 percent (2021) and 5.3 percent (2022), mainly thanks to the instrument of short-time work. The pre-crisis level of employment is expected to be seen in the course of 2022.

Currently, the number of employed persons is still three-quarters of a million (1.7 percent) below the pre-crisis level. The labor force is expected to be more than 7 percent below pre-crisis levels in the first quarter, with pre-crisis labor market comparisons significantly understating the impact of the Corona crisis given the upward trends that existed previously. Without the crisis, there would be about one million more jobs today.

The inflation rate is expected to pick up to 2.3 percent in 2021, with monthly rates exceeding the 3 percent mark in the final quarter. The German government's climate package accounts for 0.4 percentage points of the increase, while the rise in value-added tax add another 1.2 percentage points. These temporary factors will phase out next year, when inflation rates are expected to fall back below 2 percent.

"The hike in this year’s inflation numbers is essentially due to temporary factors and is not yet the harbinger of a new inflation trend. This does not take the issue of inflation off the table in the medium term, but the reasons for this are to be found elsewhere, in particular in the interplay between high government debt, an aging population and unbridled monetary policy," Kooths said.

At 4.6 percent of GDP, the 2021-deficit in public budgets is even higher than last year (4.2 percent). It will fall to 1.3 percent next year as the economy recovers and pandemic-related spending is cut back. In 2022, Germany's debt level will fall below 70 percent (in relation to GDP) again after soaring by 13 percentage points during the pandemic.

"With the progressing recovery, the justification for large-scale deficit spending vanishes. Thus, there is no economic reason for an extended suspension of the debt brake. Next year’s structural public deficit exceeds the rule-based level by 40 billion euros. The new federal government will therefore face consolidation pressures from the outset, especially as the burden of demographic aging is increasing from year to year. As the country is inadequately prepared, social conflicts are likely to intensify considerably in the next legislative period," said Kooths.

Stimulus from strong US economy

The global economy is being driven not least by a stronger US economy on the back of another large fiscal stimulus. Based in purchasing power parities, global output is expected to increase by 6.7 percent in 2021 and by 4.7 percent in 2022, thus progressively closing the gap to the pre-crisis path of activity. World trade in goods is expected to grow by 7.5 percent this year. With growth of 3.7 percent next year, world trade towards the end of the forecast horizon will thus be even higher than we expected prior to the crisis.

In the euro area, gross domestic product is expected to increase by 4.8 percent this year and by 4.3 percent in 2022. This translates into topping pre-crisis levels towards the end of 2021. Economic output in the euro area is currently around 5 percent below its pre-crisis level. From the summer onwards, particularly strong growth rates are expected in trade in services, private consumption, and investment in machinery and equipment.