Joint Economic Forecast 1/2024

Headwinds from Germany and abroad: institutes revise forecast significantly downwards

"Cyclical and structural factors are overlapping in the sluggish overall economic development. Although a recovery is likely to set in from the spring, the overall momentum will not be too strong," says Stefan Kooths, Head of Economic Research at the Kiel Institute for the World Economy.

In the current year, private consumption will become the most important driving force for the economy, followed by stronger exports in the coming year.

Economic output is currently at a level that is barely higher than before the pandemic. Since then, productivity in Germany has been at a standstill. There have recently been more headwinds than tailwinds in the domestic and foreign economies.

Private consumption picked up later and less dynamically than previously expected by the Joint Economic Forecast Project Group. German exports declined despite rising global economic activity, primarily because demand for capital and intermediate goods, which are important for Germany, was weak and price competitiveness for energy-intensive goods suffered.

Ongoing uncertainty about economic policy is weighing on corporate investment, which is likely to remain at the 2017 level despite the expected upturn in the coming year.

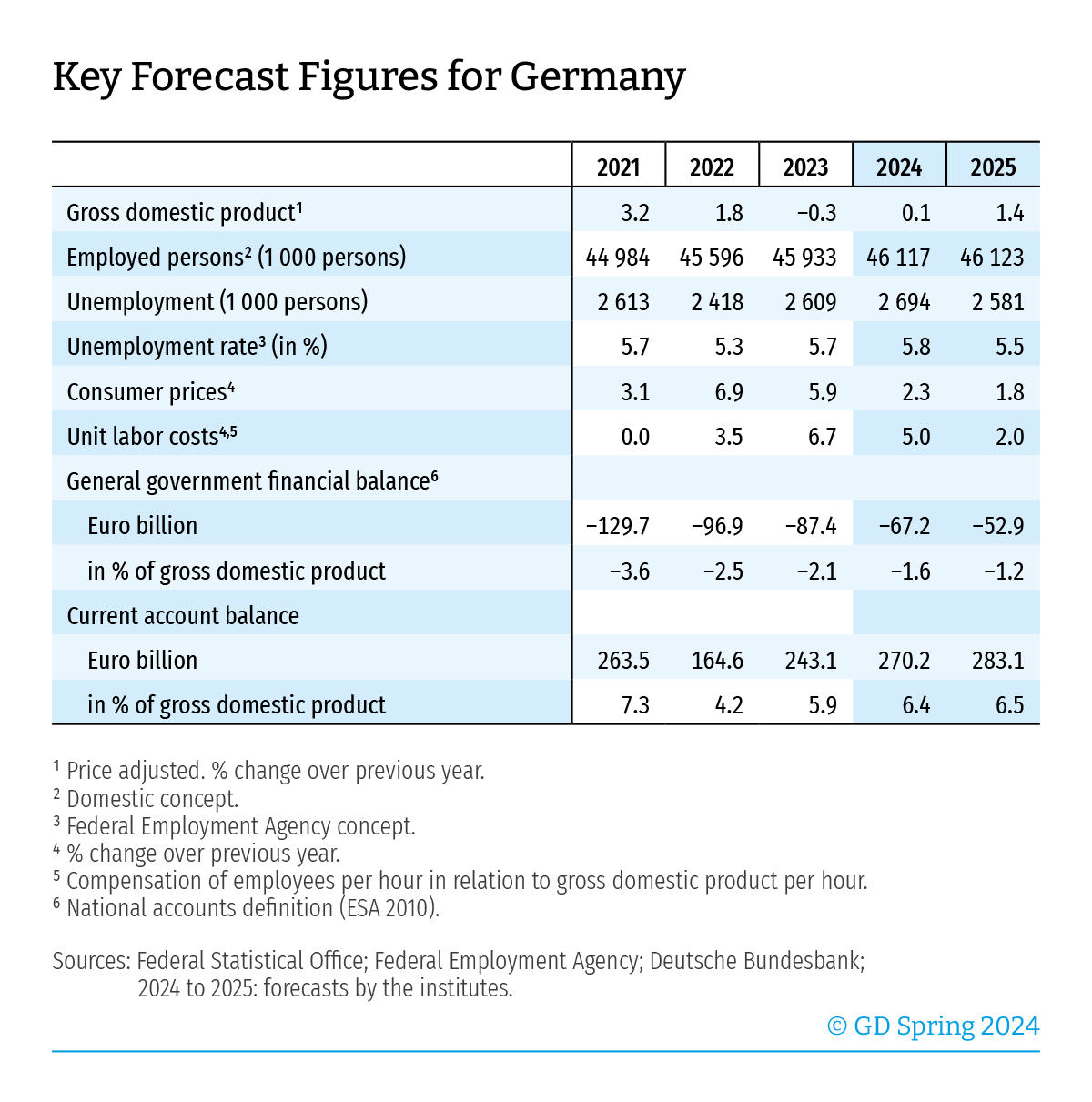

Nominal effective wages are expected to increase by 4.6 percent and 3.4 percent in 2024 and 2025 respectively. This means that real wages will increase over the entire forecast period and make up for the losses from 2022 and the first half of 2023. However, the level seen at the end of 2021, before the drastic surge in inflation, is not expected to be reached until the second quarter of 2025.

Overall, the institutes expect consumer prices to rise by 2.3 percent in the current year and by 1.8 percent in the coming year. Adjusted for the dampening effect of energy prices, core inflation rates are 2.8 percent (2024) and 2.3 percent (2025).

A robust labor market is supporting consumption-related upward forces. Although real unit labor costs are rising again significantly in the wake of wage increases, they remain supportive for labor demand.

Unemployment is likely to rise only slightly and fall again starting from spring onwards. Over the course of the year, the unemployment rate is likely to be 5.8 percent (2024) and 5.5 percent (2025).

The deficits in the general government budget in relation to economic output will fall from 2.1 percent in the previous year to 1.6 percent (2024) and 1.2 percent (2025). The public sector revenue ratio will reach record levels for Germany as a whole in the two forecast years at 47.5 percent and 48.4 percent respectively.

With regards to the debt brake, the experts recommend a mild reform. While supporting the proposal of Deutsche Bundesbank, which allows for more debt-financed investments than before, the institutes also suggest a transition phase for reactivating the deficit limit instead of an abrupt tightening.

More important, however, is a reorganization of the overall fiscal constitution in order to better shield municipal investment activity—a good 40 percent of total public investment—from cyclical budget shortfalls.

Full report (in German):

About the Joint Economic Forecast

The Joint Economic Forecast is published twice a year on behalf of the Federal Ministry for Economic Affairs and Climate Action. The following institutes partici-pated in the spring report 2024:

German Institute for Economic Research (DIW Berlin)

ifo Institute - Leibniz Institute for Economic Research at the University of Munich e. V. in cooperation with the Austrian Institute of Economic Research (WIFO) Vienna

Kiel Institute for the World Economy

Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

RWI - Leibniz Institute for Economic Research in cooperation with the Institute for Advanced Studies Vienna