Kiel Institute Highlights

How China lends - a rare look into 100 debt contracts with foreign governments

The Chinese government is the world’s largest official creditor, but we lack basic facts about how China and its state-owned banks and enterprises lend. In a recent study jointly conducted with researchers from AidData, the Center for Global Development, and the Peterson Institute for International Economics, we provide the first systematic analysis of how Chinese creditors write loan contracts and of the terms and conditions they contain. We show that Chinese loans have unusual secrecy provisions, collateral requirements and creditor friendly cancellation and acceleration rights.

Neither Chinese creditors nor their sovereign debtors normally disclose the text of their loan agreements. But the legal and financial details in these agreements have gained relevance in the wake of the COVID-19 shock and the growing risks of financial distress in countries heavily indebted to Chinese lenders. In light of the high stakes, the terms and conditions of China’s debt contracts have become a matter of global public interest.

The first systematic study to evaluate China’s debt contracts abroad

In our study (Gelpern et al., 2021), we examined 100 Chinese loan contracts to 24 countries, many of which participate in the Belt and Road Initiative. The analysis is the first systematic evaluation of the legal terms of China’s foreign lending, and the newly published contract dataset is the largest source of debt contracts between Chinese government lenders and developing country borrowers. These documents were difficult to access, but over a 36-month period AidData collated the contracts by conducting an in-depth review of the debt information management systems, official registers, and parliamentary websites of 200 borrower countries. We benchmarked the Chinese contracts against 142 publicly available contracts with other major lenders and found several unusual features in Chinese contracts.

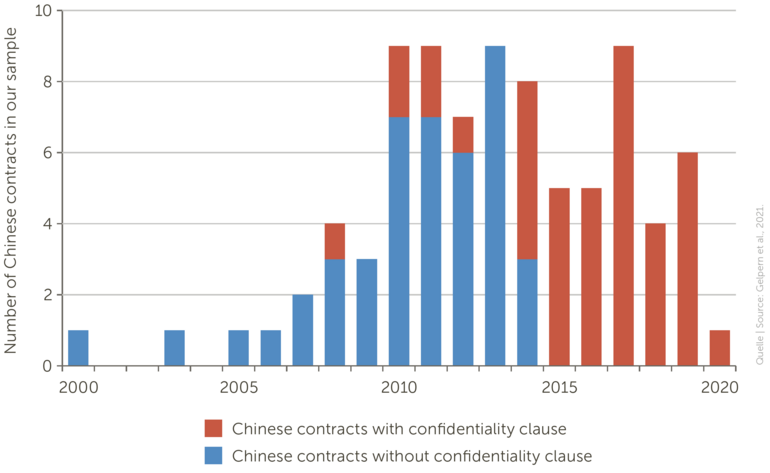

China’s contracts contain unusually broad confidentiality clauses, which prevent borrowers from revealing the terms or sometimes even the existence of the loans. These confidentiality clauses create “hidden debt” issues in the developing world that hamper debt sustainability assessments and the pricing of risks (also see Horn et al., 2021). Most importantly perhaps, they hide loans from the people that are bound to repay them via taxes and make it difficult for the public to hold government accountable. China’s contracts have also become more secretive over time, with a confidentiality clause in every contract in the dataset since 2014.

Chinese creditors want to be senior

The contracts also contain provisions that position Chinese state-owned banks as senior creditors whose loans should be repaid on a priority basis. Nearly a third of the contracts required borrowing countries to transfer proceeds from commodity exports or the profits from underlying projects to offshore bank or escrow accounts. These informal collateral arrangements put Chinese lenders at the front of the repayment line since the Chinese banks can simply dip into their borrower’s accounts to collect unpaid debts. Many of the contracts also contain clauses that exclude Chinese debt from multilateral debt restructuring initiatives and therefore restrict the borrowing countries’ options in case of repayment difficulties.

Use of confidentiality clauses in Chinese contracts over time

Loan agreements as a vehicle to extend political influence

Finally, China’s contracts give it broad latitude to cancel loans or accelerate repayment if it disagrees with a borrower’s policies. For example, China Development Bank (CDB) treats termination of diplomatic relations with China as an “event of default.” Expansive cross-default and cross-cancellation provisions also provide Chinese lenders with more leverage over borrowers and other creditors than was previously understood. In addition to addressing repayment risk, this leverage could also be used by Chinese creditors to influence the borrowing country’s domestic or foreign policies.

Overall, our analysis shows that China is a muscular and commercially-savvy creditor to developing countries. By using creative contractual designs, Chinese lenders try to overcome enforcement hurdles and deal with macroeconomic and political risks in the borrowing countries. These techniques can help to increase capital flows to high-risk developing countries (Lucas, 1990). Some clauses, however, come with significant negative externalities to other creditors and will pose a challenge to multilateral cooperation, in particular during times of debt distress.

Related Publication

References:

Gelpern, A., et al. (2021). How China Lends: A Rare Look Into 100 Debt Contracts with Foreign Governments. Peterson Institute for International Economics, Kiel Institute for the World Economy, Center for Global Development, and AidData at William & Mary.

Horn, S., C. M. Reinhart und Christoph Trebesch (2021). China’s Overseas Lending. Journal of International Economics (133) 103539.

Lucas, R. E., Jr. (1990). Why Doesn’t Capital Flow from Rich to Poor Countries? The American Economic Review 80 (2): 92–96.