US employment reaches pre-crisis level but labor market is still weak

The nonfarm payroll employment level in the United States is now close to its January 2008 pre-crisis level.

The nonfarm payroll employment level in the United States is now close to its January 2008 pre-crisis level. [In this document we refer to total nonfarm payroll employment taken from the Establishment Data of the Bureau of Labor Statistics, which is the most cited employment figure for the United States.] The consensus forecast expects an increase in employment of roughly 200,000 from April to May of this year. If this forecast turns out to be correct, employment in May will have exceeded its pre-crisis level of 138,365,000 employees, thereby reaching a new all-time high in absolute numbers. However, the fact that employment will have exceeded its pre-crisis level does not indicate strength in the labor market but, rather, ongoing weakness. While employment is roughly at its pre-crisis level, the civilian noninstiutional population (16 and over) has increased by more than 15 million over the same period. As a result, employment as a share of the population has decreased dramatically, with few signs of recovery. [The same picture emerges when looking at the employment-population ratio from the Current Population Survey.]

Even though employment as a share of the population has remained at its lower level, the unemployment rate has fallen precipitously, from a post-crisis high of about 10 percent of the labor force to a level between 6 and 7 percent. This strong decline in the unemployment rate from its post-crisis high has been mainly driven by the decline of the participation rate. This decline means that a large number of people, on the net, have left the labor force. Overall, it seems that the events surrounding the financial crisis may have had permanent negative effects on employment levels, such that employment levels have now begun to follow a lower trend growth path than before the crisis.

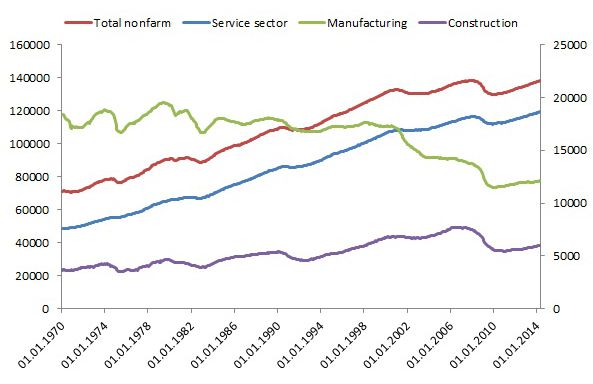

This picture also emerges when looking at sectoral employment developments, even though there are noticeable differences across sectors. The strongest rebound in employment has taken place in the service sector as a whole, in which more than 7 million jobs have been created after the post-crisis trough. As a result, employment in the service sector now sits at more than 2 percent above its pre-crisis level, which is a fall relative to pre-crisis trends. Meanwhile, in the manufacturing sector, only 1.4 million jobs have been created after the post-crisis trough, out of more than 4 million jobs lost during the crisis. As a result, employment in the manufacturing sector now sits at more than 10 percent below its pre-crisis peak. Not surprisingly, the construction sector has performed even more poorly, with an employment level still 20 percent below its pre-crisis peak. In all three sectors, a permanent downward shift in employment has apparently taken place relative to pre-crisis trends, with the construction sector most affected by the crisis (Chart 1).

Chart 1: Employment in the United States 1970-2014 (thousand persons)

Source: Establishment Survey, Bureau of Labor Statistics.

While the aggregate employment situation remains dismal, in relative terms, some sectors have done better than others. In relative terms, there appear to be some possible signs of reindustrialization. According to some reports, this relative reindustrialization may have been stimulated by the so-called “shale gas revolution”, alongside other developments. Employment in the mining and logging sector, which is directly related to the increase in shale gas (or shale oil) production, is well above its pre-crisis level both absolutely and in relation to overall employment (Chart 2). Moreover, the share of manufacturing employment in total employment has also stabilized, relative to its previous downward trend. However, these signs of reindustrialization are apparently too small to result in significant improvements to the overall labor market.

Chart 2: Sectoral shares in total employment in the United States 1995-2014 (Share in total nonfarm employment)

These assessments are supported by a more formal analysis which decomposes recent employment developments into three sets of shocks: (a) a set of common business cycle shocks, and sets of permanent shocks to hit (b) the overall labor market and (c) specific sectors of the labor market, relative to their long-run trends (Reicher 2014b). [This analysis is a simplified extension of the more extensive analysis conducted by Reicher (2014a).] Based on this last set of shocks in particular, the decomposition suggests that employment in the manufacturing sector and in the mining and logging sector has contributed disproportionately to recent employment growth, relative to its predicted behavior. However, the decomposition suggests that, altogether, employment remains considerably lower than it would have been in the absence of sector-specific shocks. This is because negative shocks to construction in particular, along with a few other sectors, were more than large enough to offset positive developments in mining and manufacturing. Altogether, the analysis suggests that employment is about 2 percent below the level that would have prevailed in the absence of these sector-specific shocks. Furthermore, this shift is on top of a large, permanent, negative symmetric shock to the overall labor market, to the point that employment as a share of population is now at or near its new, lower, trend. Altogether, these results are in line with other results that show that the crisis has resulted in a permanently lower level of economic activity (Jannsen and Scheide 2010).

In conclusion, an analysis of employment at the sectoral level suggests that the labor market in the United States is still in a poor shape, even though employment has reached its pre-crisis level. There is strong evidence that a large portion of the weak employment situation has resulted from a permanent decline in overall employment, with some sectors contributing disproportionately to the decline. While there are some signs of reindustrialization in relative terms, this reindustrialization has been too weak to counteract these negative shocks. These results have implications for the conduct of monetary policy, since monetary policy is mainly equipped to deal with transitory shocks rather than permanent shocks. [This assessment is in line with the results of Jannsen and Scheide (2011a, 2011b), who analyze the response of monetary policy to permanent output losses following the crisis in the United States. Ongoing work at the IfW has looked at similar issues with respect to the conduct of fiscal policy.] Since employment and unemployment are near their new trends, other policy measures may be needed to increase the labor force participation and employment rates.

References

- Reicher, C. (2014a). "The aggregate effects of long run sectoral reallocation". Kiel Working Paper 1928.

- Reicher, C. (2014b). "Sectoral reallocation and slow recoveries". In progress.

- Jannsen, N. and J. Scheide (2010). Growth Patterns After the Crisis: This Time is not Different. Kiel Policy Brief 22. Kiel Institute for the World Economy.

- Jannsen, N. and J. Scheide (2011a). Is Monetary Policy in the United States Too Expansionary? Kiel Institute Focus 8. Kiel Institute for the World Economy.

- Jannsen, N. and J. Scheide (2011b). Ist die Geldpolitik in den USA zu expansiv ausgerichtet? Kiel Policy Brief 26. Kiel Institute for the World Economy