Policy Article

Japan as an External Creditor and Internal Debtor: Are These Positions Sustainable?

Traditionally and for a long time, Japan has been both one of the world's largest external creditors (as measured by its current account surplus) and the world's largest debtor against its own citizens (as measured by the record-high gross government debt/GDP ratio of about 220 percent). In 2011, the Fukushima shock followed by temporary breakdowns of cross-border supply chains and losses in export revenues together furthered yen appreciation, and rising imports of fuels led Japan for the first time since 1980 into a trade deficit. 2012 will not show a recovery into a surplus. Nor is it expected that the domestic debt situation will visibly improve.

Traditionally and for a long time, Japan has been both one of the world's largest external creditors (as measured by its current account surplus) and the world's largest debtor against its own citizens (as measured by the record-high gross government debt/GDP ratio of about 220 percent). In 2011, the Fukushima shock followed by temporary breakdowns of cross-border supply chains and losses in export revenues together furthered yen appreciation, and rising imports of fuels led Japan for the first time since 1980 into a trade deficit. 2012 will not show a recovery into a surplus. Nor is it expected that the domestic debt situation will visibly improve.

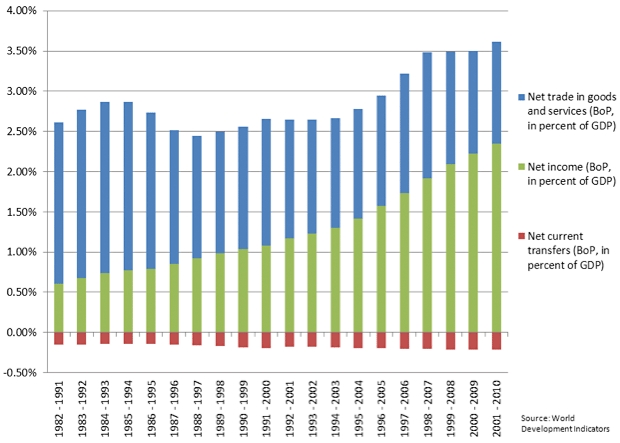

One is tempted to describe the deterioration of the Japanese trade account as a temporary event pushed by a combination of external shocks like Fukushima and exchange rate movements toward appreciation driven by the use of the yen as a "carry trade" currency. However, this view may be misleading. A look at the composition of the Japanese current account and its three components (net exports of goods and services (trade), net investment income and transfers) over a longer time period by using 10-year moving averages reveals trends rather than short term fluctuations. These trends show that since the mid-1980s, this composition has markedly changed (see Figure (Note 1)). The trade component (blue bar) declined in importance while the net investment income component (green bar) rose in importance. The transfer component (red bar) influenced by Japanese development aid contributions rather than worker remittances remained relatively unimportant and constant. Compared to other industrialized economies, such as Germany or the United States, this is a rather unique pattern. In these two countries, the trade component still dominates on the surplus or deficit side, respectively. Yet, it mirrors similar developments in France and Italy, two countries with severe problems of international competitiveness of the home base. Thus, the shift in the composition of the Japanese current account could give rise to the following observations and questions:

- As a mature and aging economy, the growth of the Japanese economy seems increasingly better portrayed by the growth of its gross national product (which includes net factor income earned abroad) than by the growth of its gross domestic product which stands for value added generated within the national boundaries.

- Japan has always been a more important exporter of private risk equity capital (foreign direct investment and portfolio investment) rather than a host of such foreign capital. This is why net investment income earned by foreign investors in Japan and repatriated home has always been by far lower than net investment income earned by Japanese investors abroad and repatriated home.

- Assumed Japanese growth remains as its "steady state rate of growth" of about 1 percent and assumed the Japanese government tries to sustain the servicing of the huge domestic debt by broadening the domestic tax base (and/or increasing the tax rates such as doubling the VAT over the next three years), how will the Japanese private sector react? Will it then prefer overseas investment rather than domestic investment because of fears that rising taxation will stifle domestic demand, and if it would decide against the latter and in favor of overseas investment, would it continue to repatriate investments returns or would it reinvest them in the host countries?

An answer to the latter question is decisive for the sustainability of the current trend of net foreign investment repatriated to Japan as the most important backbone of the Japanese current account to remain still in surplus. There are special events which drive Japanese foreign investment income home in order to rebuild the domestic capital stock. That happened after the Great Hanshin earthquake in 1995 and it was repeated after the Fukushima accident. But regardless of such special events, it cannot be excluded that the gap between international rates of return on risk capital and domestic rates of return in Japan will rise in the future and that such gap will not be fully (or not all) compensated for by a depreciation of the yen which makes the home production base internationally more competitive. The question is whether the gap will grow or shrink. A growing gap (after adjusted by exchange rate changes) would be bad news for the current account to remain in surplus. A shrinking gap, however, could induce Japanese investors to launch domestic investment perhaps at the expense of foreign investment and for investors already acting abroad to decide against reinvestment in the host country and instead repatriating the returns: good news for the Japanese current account. It could also induce foreign investors to come to Japan and to reinvest their returns there. This would also shift the net investment income into a surplus direction.

Both directions of the gap are dependent on the world economic development (on which Japan has very little influence) and on the Japanese economic development ( on which the country has full responsibility by either pushing or delaying reforms which could be instrumental to improve the country's position in the "beauty contest" for foreign investors).

Arguments pro declining gap are:

- An expected period of fiscal consolidation faced by Europe and the United States accompanied by an extra-cyclical decline in the economic growth in China and South Korea. In the case of China, rapid investment-driven growth comes to an end and will be substituted for a by less rapid innovation-driven growth. This period will show slower growth, more risk aversion in investment, more resistance of banks against imprudent lending and thus also less product innovation. This could bring international rates of return on investment down.

- A stronger home bias of Japanese investors triggered not only by the needs to rebuild the domestic energy base after the Fukushima accident but eventually also by the decision of Japanese companies to cut the length of cross-border value added chains and to raise the domestic content in the manufacturing process. Such decisions could be driven by a number of factors, such as rising costs of trade finance in a cyclical downturn, rising domestic excess capacities, concerns to become the victim of discrimination after political conflicts among Asian neighbors, or a stop in the appreciation trend of the yen following the example of the Swiss Central Bank to put an upper cap on the nominal exchange rate.

Arguments pro growing gap are:

- An asymmetric business cycle between Japan (remaining in a cyclical trough) and the rest of the world enjoying an upswing. Such asymmetries could come from a number of factors, such as rising commodity prices, a structural shift in world demand towards services which are not the export champions of Japan, or the acceptance of China to assume the role of a benevolent hegemon in international trade and the global financial architecture by shouldering part of the burden of adjustment of third countries.

- A loss in confidence of Japanese companies in the reform willingness and reform capacity of Japan relative to alternative investment in the rest of the world.

Which of the two alternatives are plausible or more likely than the other and which implications would that have for the servicing of public debt?

In my view, I see more arguments for a declining gap in the foreseeable future. In principle, these were good news for Japan and the capacity of the Japanese government to service the public debt. It provides breathing space for the country. However, for such good news to sustain rather than resulting only from a positive random coincidence of some spurious factors in the world economy, it requires massive reforms in Japan to accelerate structural change. The reason why I see a declining gap is the large likelihood of a longer phase of fiscal consolidation and slower growth and the end of rapid growth in emerging economies in the world economy. This phase would also face the unsolved issue of the future of sovereign debt in Europe and the doubts whether the United States will survive as the number one international currency (without the Chinese renminbi (RMB) already prepared to take over). All taken together, such factors can drive risk premia upward and can bring international rates of return down.

At the same time, Japan will be forced to rebuild destroyed capacities, manage a change in its energy policy and reinvest in the capital stock of its public infrastructure. Thus, in comparison to the past, Japanese investors will have more incentives to repatriate their investment income earned abroad and invest at home. In doing so, they would contribute to broaden the domestic tax base and facilitate the servicing of domestic debt through taxation of the private sector. However, such tail wind from the world economy can be spurious and volatile. Additional tail wind from the domestic policy frontier is required. Such policies, for instance, would encompass a society-wide agreement on an immigration policy under criteria of economic benefits for Japan, or a strategy to cut the high costs of starting a business in Japan (Note 2). All of that requires a cultural sea change in Japan. Such sea change is difficult and will take time, but its urgent need must be disseminated by the government to the electorate. History suggests that dissemination of such crucial reforms outside war times needs a statesman even prepared to lose the next election rather than a simple incumbent in office. Otherwise, temporary tail wind or breathing space from the world economy will fade out without having helped Japan to use its current account surplus for servicing its domestic debt.

Notes:

- This figure has been taken from Rolf J. Langhammer, "The Importance of Investment Income and Transfers in the Current Account. A New Look on Imbalances. Kiel Policy Brief, No 48, May 2012.M

http://www.ifw-kiel.de/wirtschaftspolitik/politikberatung/kiel-policy-brief/KPB_48.pdf - See the 114th rank of Japan in the 2013 World Bank Study "Doing Business")

http://www.doingbusiness.org/data/exploreeconomies/japan

(First published on the website of the Research Institute of Economy, Trade & Industry (RIETI), http://www.rieti.go.jp/en/special/p_a_w/021.html?stylesheet=print.).

Key Words

- Japan