Working Paper

Interconnectedness in the Global Financial Market

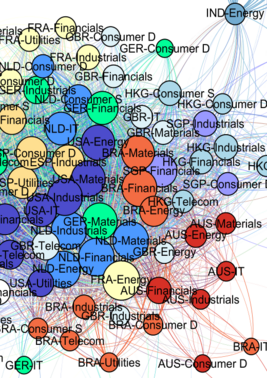

The global financial system is highly complex, with cross-border interconnections and interdependencies. In this highly interconnected environment, local financial shocks and events can be easily amplified and turned into global events. This paper analyzes the dependencies among nearly 4,000 stocks from 15 countries. The returns are normalized by the estimated volatility using a GARCH model and a robust regression process estimates pairwise statistical relationships between stocks from different markets. The estimation results are used as a measure of statistical interconnectedness, and to derive network representations, both by country and by sector. The results show that countries like the United States and Germany are in the core of the global stock market. The energy, materials, and financial sectors play an important role in connecting markets, and this role has increased over time for the energy and materials sectors. Our results confirm the role of global sectoral factors in stock market dependence. Moreover, our results show that the dependencies are rather volatile and that heterogeneity among stocks is a non-negligible aspect of this volatility.

Key Words

- Asset markets

- Comovement

- financial networks

- Interconnectedness