News

Kiel Institute Summer Forecast: Light at the End of the Tunnel

The downturn appears to have bottomed out. “Leading indicators support our view that, after two years of contraction, the industrial sector has reached the trough—albeit at a low level,” says Stefan Kooths, Head of Forecasting at the Kiel Institute for the World Economy. “The recovery is largely being driven by domestic factors. After a two-year drought, private consumption is rising noticeably again, and corporate investment is beginning to pick up.”

Still, private-sector momentum remains weak for this stage of recovery. However, next year, the significantly greater fiscal room for the new federal government is expected to accelerate the pace of expansion—though this will come at the cost of rising public debt.

Forecasts at a glance:

- German economy in summer 2025: Signs of recovery as economy bottoms out

- World Economy in Summer 2025: Trade policy headwinds - slower expansion

“Trade policy risks remain substantial,” says Moritz Schularick, President of the Kiel Institute. “The erratic tariff policy of the United States continues to fuel uncertainty for German foreign trade.” In addition, German exporters are still hampered by significantly reduced competitiveness.

Exports falter, private consumption rises

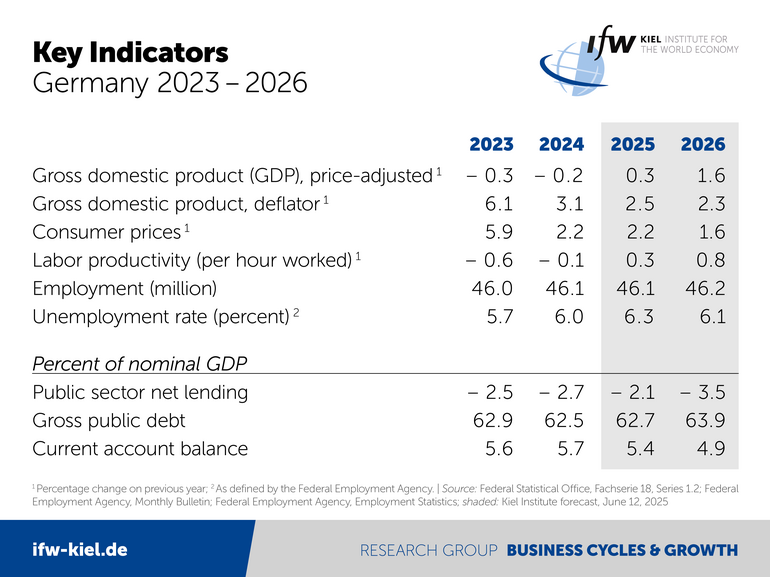

Exports are expected to contract by 0.4 percent in 2025, before rebounding by 1.2 percent in 2026. While private consumption won't sustain the strong momentum seen earlier in the year, it is projected to rise by around 1 percent in both years.

Private investment in equipment, which has been declining for two years, is set to recover this year and grow by 3.5 percent in 2026. Government investment in equipment—particularly in military procurement—is expected to rise by around 15 percent annually. Construction investment, after hitting a low point last year, is also rebounding, with a projected increase of 1 percent in 2025 and 3 percent in 2026.

Falling unemployment, rising debt

The slightly brighter outlook is also reflected in the labor market. Although the unemployment rate is projected to rise slightly from 6.0 percent in 2024 to 6.3 percent this year, it should fall back to 6.1 percent by 2026.

Core inflation (excluding energy) will remain above 2 percent, but falling energy prices and fiscal measures are expected to bring the overall inflation rate down to 1.6 percent in 2026 (from 2.2 percent this year).

As the new government takes a more expansionary fiscal stance, the public deficit is projected to increase to 3.5 percent of GDP in 2026. For 2025, consolidation efforts and provisional budget measures will keep the deficit lower at 2.1 percent (2024: 2.7 percent). The debt-to-GDP ratio is expected to rise from 62.5 percent in 2024 to 63.9 percent in 2026.

Global economy: moderate growth

According to the Kiel Institute, the global economy is expected to grow by 2.9 percent this year and next—noticeably slower than in the previous two years. The slowdown is primarily driven by a marked loss of momentum in the United States, while China's economy continues to lack dynamism. In contrast, the European economy is expected to see a modest recovery.