News

Kiel Institute Economic Outlook: Upswing Not In Sight Until 2021 at the Earliest

The economic downturn in Germany is being driven by the recession in industry, where capacity utilization is now below normal, but providers of business-related services are more and more affected. "The downward momentum is weakening, and foreign sales even seem to have turned around already. Experience has shown, however, that it takes five quarters on average before industry overcomes a recession and capacity utilization increases noticeably again. This means that the earliest time to expect this to happen is in the second half of 2020, and only then can the economy as a whole start a significant upturn again. For the time being, the German economy will crawl into the new year," said Stefan Kooths, Head of the Forecast Centre at the Kiel Institute for the World Economy (IfW Kiel).

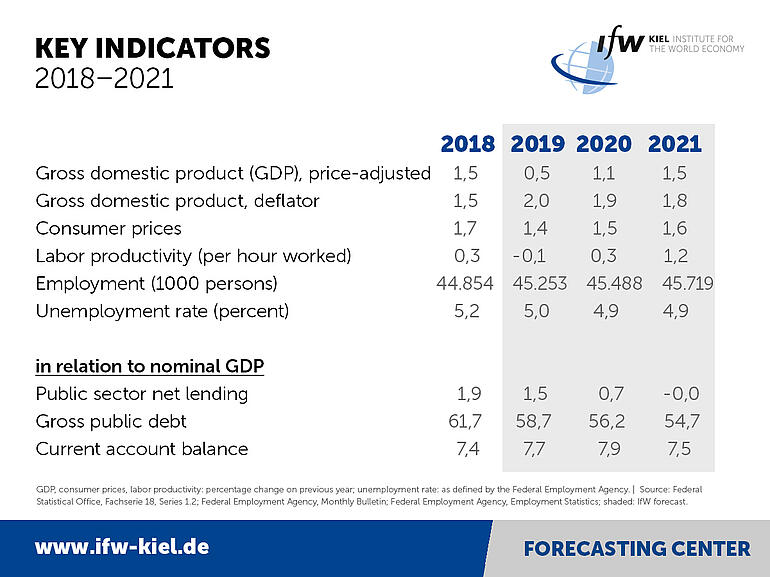

The global economy is likely to gradually pick up in the course of next year, led by developments in emerging economies where expectations have already started to brighten up. World output measured at purchasing power parities should rise by 3.0 percent (2019), 3.1 percent (2020) and 3.4 percent (2021). "Growth in 2019 and 2020 would be the lowest since the Great Recession in 2009. Even lower growth would result in the case of a further significant deterioration of the environment for international trade leading to an additional slowdown of investment, for example ifthe crisis at the WTO was to intensify," said Kiel Institute President Gabriel Felbermayr.

Domestic economy counteracts industrial recession

The downturn in Germany particularly visible in corporate investments, which are expected to fall by 1.1 percent in 2020 after growth of 1.2 percent this year.. Only in 2021, in the wake of the economic recovery, can a moderate increase of 2.3 percent be expected.

While industry is in recession, activity in more domestically oriented parts of the economy such as services and construction continues to increase. As a result, capacity utilization in the economy as a whole will next year fall below its normal level only slightly . The construction industry will continue to be fueled by extremely favorable financing conditions. After 3.9 percent this year, construction investments are expected to grow by 2.5 percent in each of the next two years. Private households are benefiting from numerous fiscal measures and from a robust the labour market supporting private consumption growth of 1.5 percent this and next and 1.7 percent in 2021. The inflation rate will remain stable at 1.4 percent (2019), 1.5 percent (2020) and 1.6 percent (2021).

The labour market benefits from the fact that more employment is still being built up in consumer-related services than is being lost in industry. The unemployment rate is likely to remain close to this year’s level of 5 percent, at 4.9 percent, over the next two years. "Overall, employment growth is slowing down and employment risks have risen, partly because real unit labour costs are no longer supportive," Kooths said.

Government balance 2021 negative

After a record surplus in public budgets of almost 62 billion euros in 2018, the surplus in 2019 should still be significant, albeit lower, at 53 billion euros. In 2020, the budget surplus is likely to fall to 24,3 billion euros and finally become negative in 2021 at -1,7 billion euros. Kooths: "The partial abolition of the “Soli” reduces revenues, which will not be matched by the revenues from the planned new CO2 tax. At the same time, the introduction of the basic pension and the implementation of the climate package will lead to additional expenditures.

The economic development in the German export markets remains subdued as the US economy will continue to lose momentum in 2020 and the trend of a gradual slowdown in China will persist. Although German exports are picking up only moderately to 2.4 percent (2020) and 2.6 percent (2021after an increase of 1.2 percent (2019)), they are expected to catch up with world trade again.

"Germany does not need an economic stimulus package”

"Despite the current weakness, the German economy does not need an economic stimulus package. The industrial recession has its causes largely in the foreign trade environment and would hardly react to domestic government stimulus," Kooths said.

"In the medium term, however, there is much to be said for giving greater priority to investment spending in the national budget. The debt brake does not stand in the way of this, but forces to clarify its priorities. If infrastructure, schools, etc. have a high priority, other areas must necessarily be less important. New debt does not finance the positions at the top of the priority list, but what would be omitted at the bottom. In the worst case, necessary but unpopular reforms would only be delayed by new budget deficits."