News

Kiel Institute Economic Outlook: German upswing loses momentum

"The catch-up process remains intact but slows down during the winter term," comments Kiel Institute head of forecasting Stefan Kooths on the economic outlook for Germany, the euro area and the global economy published today.

Overall, the Covid-19 crisis is estimated to cost the German economy EUR 320 billion in terms of loss of economic output in the years 2020 to 2022. The supply-side bottlenecks are expected to dampen value added in the manufacturing sector by more than EUR 40 billion this year, much of which is likely to be made up once the bottlenecks are overcome.

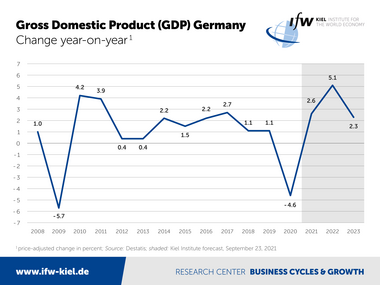

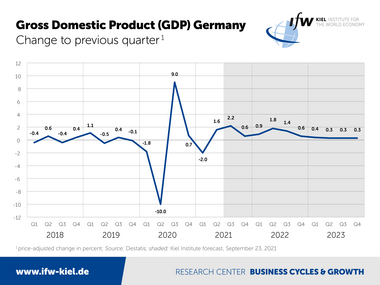

With the recovery initially weaker, the German economy is not expected to reach its pre-crisis level until the first quarter of 2022, half a year later than previously anticipated. From the middle of next year onwards, production capacities are likely to be utilized normally again. As a result of the stronger momentum in the coming year, economic activity will then catch up towards the end of 2022 to the level expected in the summer forecast.

"The stimulus for the interim spurt during next year is triggered by fading frictions that prevent the economy from growing faster. As the pandemic finally subsides, large parts of the contact-intensive service sectors will return to normal operations, and once the supply bottlenecks have been overcome, the record order backlog in the manufacturing sector can be worked off," says Kooths. “Consumers have plenty of purchasing power and companies' order books are full to bursting - this is what a self-sustaining recovery looks like. In this situation, further economic stimulus programs would add fuel to the fire and ultimately have a destabilizing effect by pushing the economy into overheating."

"The gap between incoming orders and industrial production is widening and is currently assuming historically unprecedented dimensions, primarily due to a lack of primary products. Outside the ports of Los Angeles and Ningbo-Zhoushan alone, 6 percent of global freight capacity is currently tied up in congestion. This is bad for German economic performance and drives up prices," said Kiel Institute President Gabriel Felbermayr.

Inflation pressure remains high, employment reaches peak due to demographic factors

Private consumption is expected to increase at a rate of almost 8 percent next year, the strongest growth in recent economic history. During the pandemic, purchasing power of more than 200 billion euros has been accumulated, further reinforcing the already expansionary return to normal consumption patterns.

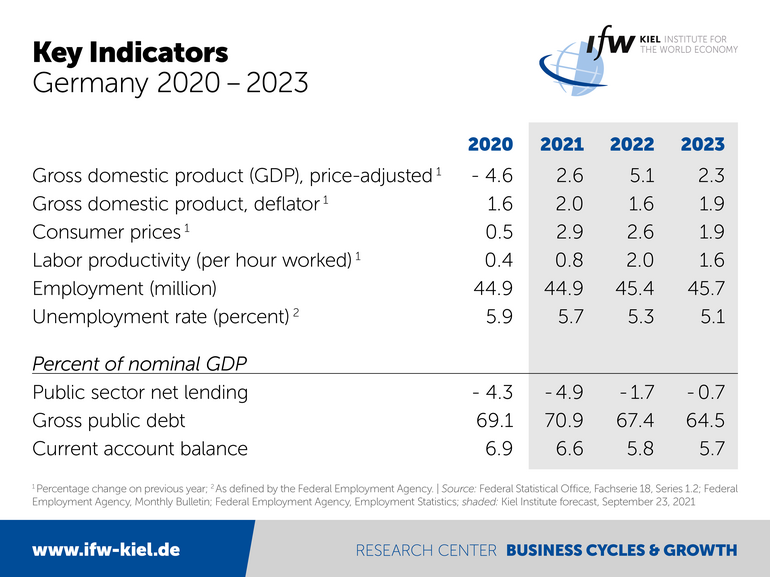

Consumer prices are rising at a rate of 2.9 per cent this year, the strongest rate in almost thirty years, with the pace of inflation accelerating in the second half of the year and likely to top 4 per cent. Although a number of specific factors fade out in the coming year, inflationary pressure will ease only gradually and the inflation rate will not fall below the 2 percent mark again until 2023.

Although the dip in the catch-up process will temporarily dampen the pace of job creation, the general picture of the labor market points to a fairly rapid recovery from the Covid-19 crisis. However, due to demographics, the economically active population will reach its peak in 2023 and from then onwards, the labor force will start to shrink significantly year by year.

The unemployment rate is expected to fall from 5.7 percent this year to 5.3 percent next year. In 2023, it is likely to fall further to 5.1 per cent, which is almost as low as the pre-crisis level.

As manufacturing picks up in the coming year, exports and investment may also pick up more strongly again. Exports are expected to grow at rates of 8.1 percent in the current year and of 5.8 and 4.2 percent in 2022 and 2023, respectively. Corporate investment is expected to increase by 6.2 and 4.6 percent in the next two years, following 3.1 percent in 2021.

Fiscal deficit declines, social security contributions rise

The fiscal deficit will rise again this year, from 145 billion euros to a good 173 billion euros (4.9 percent of GDP). The main reason is that many aid funds and subsidies for the economy to cope with the Covid-19 crisis will only flow or be called up this year. From next year on, government budgets start to recover from the Covid-19 impact. During the recovery, government revenues will rise, and extra funds will also flow in from the "Next Generation EU" program.

The deficit will then fall to a good EUR 60 billion in 2022 (1.7 percent/GDP) and to just under EUR 30 billion in 2023 (0.7 percent/GDP). In contrast, social security funds are likely to face increasing challenges and the tax burden will rise. "Not much can be done to avoid a significantly higher pension contribution rate. As planned, the contribution rate to unemployment insurance will also rise, and some health insurances are likely to adjust their additional contributions as statutory subsidies are reduced," Kooths said.

High inflation also in the euro area

For the euro area, the Kiel Institute expects a sustained normalization of social life and business conditions leading to stronger economic performance once again. GDP is expected to increase by 5.1 percent in the current year, followed by 4.4 percent (2022) and 2.4 percent (2023). Consumer prices are likely to rise quite strongly by 2.2 percent in the current year due to numerous temporary factors and base effects. In subsequent years, inflation is likely to be below the European Central Bank's inflation target again at 1.8 per cent (2022) and 1.7 per cent (2023).

The momentum in the global economy slowed significantly in the first half of 2021 as a result of new Covid-19 surges and supply chain issues, but the strong upward trend remains intact. Global output is expected to grow by 5.7 per cent this year (previous forecast: 6.7 per cent) and by 5 per cent next year (previously 4.8 per cent). Global economic activity is also expected to grow quite strongly again in 2023 at 3.8 per cent.