News

Kiel Institute Economic Forecast: Recovery is slow

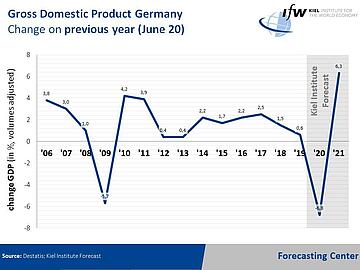

"The worst of the crisis is behind us. This is not yet the all-clear, because the low point was extremely low. This weakens the companies and burdens the recovery. The rebound in production will be more protracted than the crash. In the second quarter, gross domestic product is likely to have shrunk dramatically by 12 percent. The corona crisis thus marks the sharpest economic slump since the founding of the Federal Republic of Germany. Never before has economic activity fallen more rapidly and drastically," said Kiel Institute Economic Director Stefan Kooths on the summer forecast for Germany and the global economy up to 2021 published today.

Compared with its interim forecast in mid-May, the Kiel Institute expects the slump in the second quarter to be somewhat deeper, but now expects production to pick up again somewhat more strongly in the second half of the year, partly due to the impetus provided by the latest economic stimulus package. This is likely to lead to anticipatory effects via the reduction in VAT, especially on durable consumer goods, so that part of the stimulating effect this year will be offset by dampening effects next year (yo-yo effect). Overall, the Kiel Institute expects gross domestic product (GDP) to decline by 6.8 per cent in 2020 (interim forecast: minus 7.1 per cent) and to rise by 6.3 per cent (7.2 per cent) in 2021.

As a result of the Covid 19 pandemic, global economic activity fell by almost 10 percent in the first half of 2020, with the crisis bottoming out in April. The outlook for the advanced economies is now not quite as unfavourable as it was a few weeks ago. In 2020, global production is expected to shrink by 3.8 per cent (interim forecast: minus 4 per cent), while Kiel Institute expects a strong increase of 6.2 per cent in 2021. (6.5 percent).

Consumption collapses, savings rate soars

The measures taken by the Federal Government do not have a significant impact on the German economic picture. Contrary to other patterns, the slump was also attributable to private consumer spending, which is otherwise a stabilising factor in economic development. Following the 3.2 per cent decline in the first quarter – the largest decline in private consumption in the united Germany to date – Kiel Institute expects an even greater decline of 13 per cent in the second quarter.

The main reason for this was the lack of opportunities for consumption. As a result, purchasing power in the first half of the year alone is likely to have been reduced by almost 80 billion euros, and by as much as 130 billion euros over the full year. This shows in a sharp rise in the private savings ratio, which is expected to reach an all-time high of over 23 percent in the second quarter and 17.3 percent for the year as a whole, after 10.9 percent in 2019: "This purchasing power will be unloaded into consumer demand as soon as circumstances permit. You don't have to push the consumption, it's enough that the brakes come off," says Kooths.

Exports below pre-crisis level for the foreseeable future, current account surplus declines

In contrast, the global economic crisis is weighing stubbornly on German exports, as the global weakness in investment remains a constraining factor for German exports, which are primarily geared to capital goods, throughout the forecast period. For the year as a whole, exports are likely to fall by 12.5 percent in 2020 and rise by 8.7 percent next year, which means that they will still be well below pre-crisis levels at the end of next year. The current account surplus is falling from over 7 percent to below 5 percent in both years.

Domestically, companies are also holding back on investment, with investment in equipment and software slumping by 22 percent this year and rising by 14 percent next year. The construction industry is the least affected by the crisis. Construction investments will also increase in 2020, by 0.8 percent, and then rise more strongly again in 2021, by 2.6 percent.

Consumer prices are expected to rise by a weak 0.7 percent this year and by a strong 2.7 percent in 2021, with energy price effects and temporarily lower VAT rates shaping inflation rates. On the labor market, even the massive use of short-time work can only partially cushion the sharp decline in production. The number of employees is now falling to below 44.3 million and the unemployment rate is expected to rise from 5 percent in 2019 to 6.1 percent in 2021.

Economic stimulus package larger than 130 billion euros, fiscal stimulus less

The corona pandemic is tearing bigger holes in public budgets than any other crisis in the post-war period. The budget deficit is likely to soar to around 6 per cent of GDP (192 billion euros) this year and will still be over 3 per cent (111 billion euros) next year when revenues have stabilised and many of the aid programmes have expired. The debt ratio is expected to rise from 60 percent of GDP in 2019 to over 70 percent.

The economic stimulus package contains measures that go well beyond the 130 billion euros mentioned above. If all the items in the key issues paper are added together, the total is 170 billion euros. Apparently, the German government does not expect to be able to spend more than 130 billion euros in the current legislative period. However, the white paper does not provide sufficient information on the timing of the measures. The Kiel Institute estimates that the economic stimulus package will provide a fiscal stimulus of 80 billion euros (2.3 per cent of GDP) this year and 50 billion euros (1.4 per cent) next year.

Kooths: "The economic stimulus package contains measures on a large scale to boost mass consumption. But a lack of mass purchasing power is not the Achilles' heel of the German economy. The package will therefore fail to achieve the intended stabilisation success. Also because it is not robust against an unfavourable pandemic course. What matters now is to get the majority of companies through the coming quarters, which are still very uncertain. Through direct subsidies, not the long way around via private consumption."

This forecast is based on the assumption that the pandemic will have been largely medically overcome by spring 2021, so that economic activity will then be able to develop freely again without significant restrictions in terms of epidemic policy. Depending on whether the all-clear can be given sooner or later with regard to the risk of infection, there are up and down risks for economic development.