News

Kiel Institute autumn forecast: economy yet to gain momentum

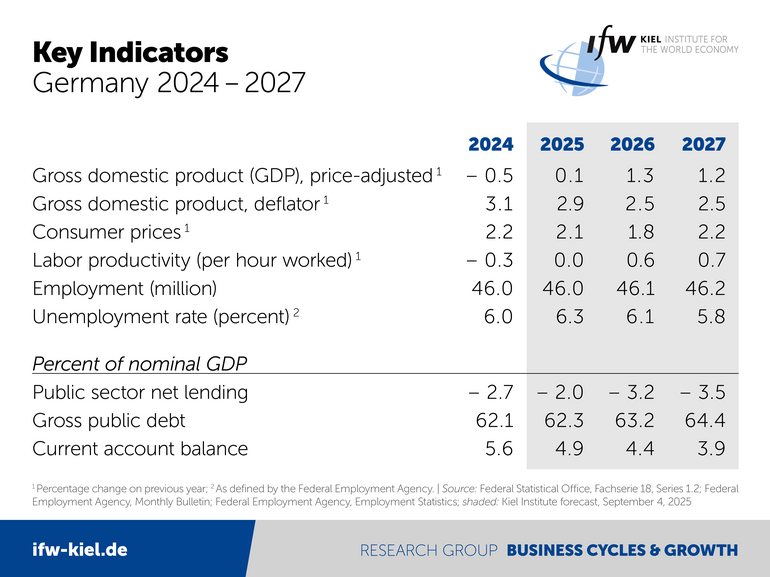

The substantially larger fiscal leeway will be used more aggressively from next year onward. While the public deficit will narrow somewhat this year, it is set to rise sharply in the following two years, thereby stimulating economic activity. Apart from these fiscal impulses, however, economic momentum remains weak. In the coming year, the high number of working days will also make a noticeable contribution to economic growth (0.3 percentage points), with overall GDP growth rates of 1.3 percent (2026) and 1.2 percent (2027). Compared with the summer forecast, this represents a slight downward revision due to lower fiscal stimulus.

“The driving forces for a self-sustaining upswing remain weak,” emphasizes Stefan Kooths, Head of Forecasting at the Kiel Institute. “Without ambitious structural reforms, the government’s aggressive deficit spending is unlikely to amount to more than a flash in the pan.”

Forecasts at a glance:

- German Economy in Autumn 2025: Economy Yet to Gain Momentum

- World Economy in Autumn 2025: Slowdown ahead

Protectionist US trade policy continues to dampen global trade and thus weighs on German exports. “German exporters are also facing increasing pressure from Chinese products on their sales markets,” explains Moritz Schularick, President of the Kiel Institute. “At the same time, Chinese imports of German goods are declining.”

Exports almost flat, private consumption picks up

Overall, German exports are likely to move sideways this year—despite the strong start to the year. In 2026 and 2027, exports are expected to grow by 0.6 percent and 1.3 percent, respectively.

Private consumption has recently stagnated after gaining noticeable momentum up to the beginning of the year. Real disposable household incomes will hardly increase this year—after rising substantially by 1.6 percent in 2024. With recovering purchasing power, private consumption is likely to pick up somewhat over the remainder of the forecast horizon. The inflation rate has recently settled close to the 2-percent mark. Over the forecast period, it is expected to trend slightly upward.

Construction investment recovers slowly

Following a recent revision of official statistics, construction investment—particularly residential construction—appears in even weaker shape. The expected bottoming out around the turn of 2025/2026 will therefore occur at an even lower level. From next year onward, construction investment is projected to recover following recent positive signals in incoming orders and building permits in the building sector. Civil engineering—driven primarily by public investment—will expand strongly throughout the period. Tax relief and government incentives are supporting equipment investment, but overall momentum remains subdued.

Unemployment falls, government debt rises

According to the Kiel Institute forecast, the expected economic recovery from next year will also bring a turnaround in the labor market: the unemployment rate is projected to decline from 6.3 percent this year to 5.8 percent by 2027. However, since the upswing is largely driven by expansionary fiscal policy, it comes at the cost of a higher budget deficit. The deficit, currently at 2.0 percent of GDP, is expected to rise to 3.5 percent in 2027.

Global economy: slowdown in 2026, moderate recovery from 2027

For the current year, global output growth—measured on a purchasing power parity basis—is expected to edge down from 3.3 percent to 3.0 percent (upward revision by 0.1 percentage points), followed by another decline to 2.8 percent next year (revised downward by 0.1 percentage points). In 2027, the global economy is expected to gradually regain momentum. Nevertheless, with growth of 3.0 percent, the increase in production will remain low by historical standards.