News

Joint Economic Forecast: Stubborn core inflation – Time for supply side policies

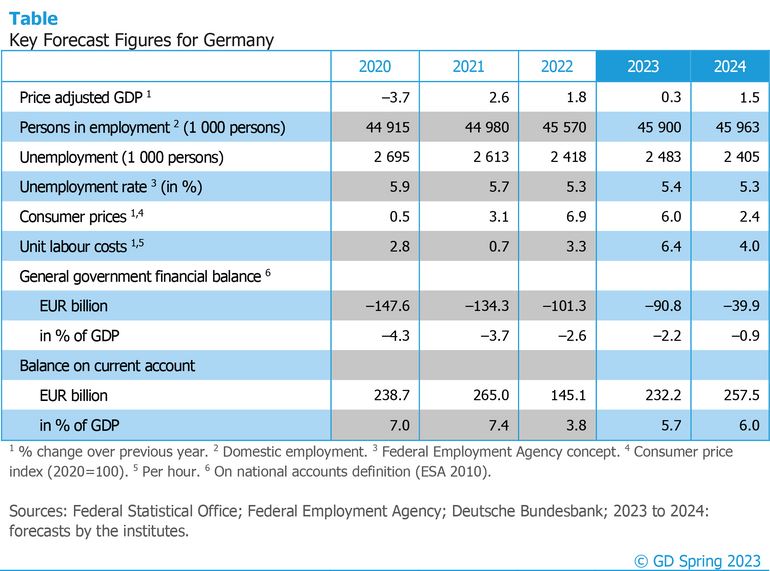

Government relief measures and foreseeably high wage increases in Germany are strengthening domestic demand and keeping domestic inflation high. Only next year will this aspect of inflationary pressure also ease, bringing the inflation rate down noticeably to 2.4 percent. Gross domestic product is then expected to grow more strongly again by 1.5 percent.

There is good news for the labor market: the number of people in employment is likely to increase again, from 45.6 million in 2022 to 45.9 million in 2023 and 46.0 million in 2024. This year, the number of unemployed will rise temporarily from 2.42 million to 2.48 million as it will take Ukrainian refugees a little time to enter the labor market. In the coming year, however, unemployment is expected to fall again to 2.41 million people.

The government will reduce its deficit only slightly to 2.2 percent of nominal GDP in the current year, since fiscal policy will remain expansionary for the time being. Only next year will policy be tightened more significantly, bringing the deficit down to 0.9 percent. A large share of the previous year’s terms-of-trade losses, which measure the loss of purchasing power in the overall economy due to the sharp rise in the price of energy imports, will be recovered by the end of 2024. As a result, the current account balance will rise again to 6.0 percent of economic output, after temporarily falling to 3.8 percent last year.

About the Joint Economic Forecast

The Joint Economic Forecast is published twice a year on behalf of the Federal Ministry for Economic Affairs and Climate Action. The following institutes participated in the spring report 2023:

- ifo Institute – Leibniz Institute for Economic Research at the University of Munich in cooperation with the Austrian Institute of Economic Research (WIFO) Vienna

- Kiel Institute for the World Economy (IfW Kiel)

- Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

- RWI – Leibniz Institute for Economic Research in cooperation with the Institute for Advanced Studies Vienna