News

Economic Outlook UPDATE: German GDP expected to slump between 4.5 and 9 percent in 2020

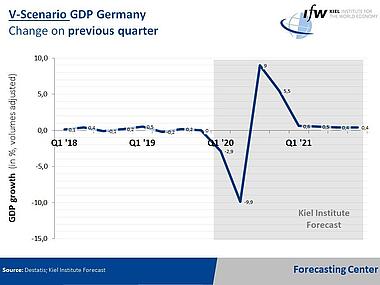

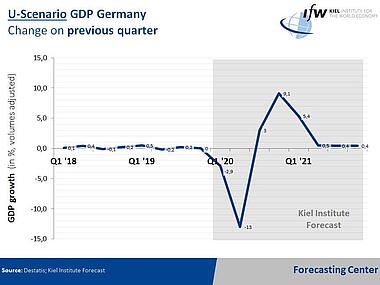

According to the V-scenario, German GDP will fall by 4.5 percent this year, assuming that the current stress situation continues until the end of April and then gradually eases from May onwards. This translates into absolute losses of value added around 150 billion euros. If the recovery sets in three months later in August, German GDP would fall by 8.7 percent.

In its spring forecast, the Kiel Institute expected a decline of GDP in 2020 of only 0.1 percent, as the massive impact on economic output in Germany caused by the global measures to contain the corona pandemic was not yet apparent in the current drama.

In both scenarios, the Kiel Institute expects GDP to fall by almost 18 percent in the second half of March compared with the previous month. This low level will probably persist until the end of April. For the further development, the Institute distinguishes a V-shape and a U-shape scenario:

- In the V-shape scenario, the dampening measures gradually subside from May onwards and the corona-related production losses subside within six months.

- The U-shape scenario envisages that the recovery will not set in before August and that production in the various sectors will not return to pre-corona levels until the beginning of next year.

Due to the global burden on the economy, both scenarios do not assume any significant catch-up effects in the further course of the year, although free capacities―especially in the manufacturing sector―would be available for this purpose.

In 2021, GDP increases strongly due to the recovery in both scenarios. In the V-shape scenario by 7.2 percent, and by 10.9 percent in the U-shape scenario.

”The U-shape scenario assumes a lockdown of large parts of economic life for almost six months, and thus goes to the limit of what is currently conceivable. Therefore, the actual development is likely to be closer to the V-shape than to the U-shape scenario,” said Kiel Institute Head of Forecasting, Stefan Kooths.

The sectors of the economy that are particularly affected, for which an initial decline in capacity utilization of 90 percent is assumed, include hotels and restaurants, aviation and the leisure industries (travel, sport, entertainment). According to this calculation, car production, as one of the heavyweights of the German economy, is now cutting back its production by up to 70 percent. Retail trade shrinks by 40 percent during the lockdown phase, with food retailers making up for some of the lost restaurant sales.

Nearly half of the German economy, however, is likely to experience little or no losses, with the real estate and housing sector, the information and telecommunications industry and large parts of the public sector (administration, education and science, homes and social services) leading the way. Thus, despite the closure of educational institutions and the resulting cancellation of teaching, there will probably no significant decline in the economic output reported in the national accounts due to the survey system of official statistics in this sector.

Apart from food retailing, essentially only the delivery services will temporarily expand their activities. In the health care sector, on the other hand, capacity utilization is likely to remain significantly higher until the end of the year.

Kooths: "This year's development is a blatant exceptional situation. The drop in production reflects a massive exogenous shock for which there are no comparable patterns in recent economic history. The slump in stock market prices and the scaling back of production processes is happening much more rapidly than during the Great Recession of 2008/2009 triggered by the global financial crisis. However, this coincides with the chance of getting out of the deep trough more quickly than ten years ago.”