News

Defaults on Chinese Debts: Developing countries risk prolonged debt overhang

"China's lending boom to developing countries seems to be coming to an end. The number of defaults and restructurings of these loans has risen strongly since 2019. Countries with high debts to China are now risking a repeat of the 1980s, when serial debt restructurings with Western creditors contributed to a lost decade and prolonged debt overhang," says Christoph Trebesch, Research Director for International Finance and Macroeconomics at the Kiel Institute for the World Economy.

Together with Carmen Reinhart, Chief Economist at the World Bank, and World Bank economist Sebastian Horn, he evaluated numerous documents and statistics from 2000 to 2021, such as official reports, press reports and datasets from research, to systematically document loan defaults and restructurings of Chinese overseas loans for the first time (Horn, Reinhart, Trebesch: Kiel Working Paper "Hidden Defaults"). China keeps its credit transactions largely hidden from the public.

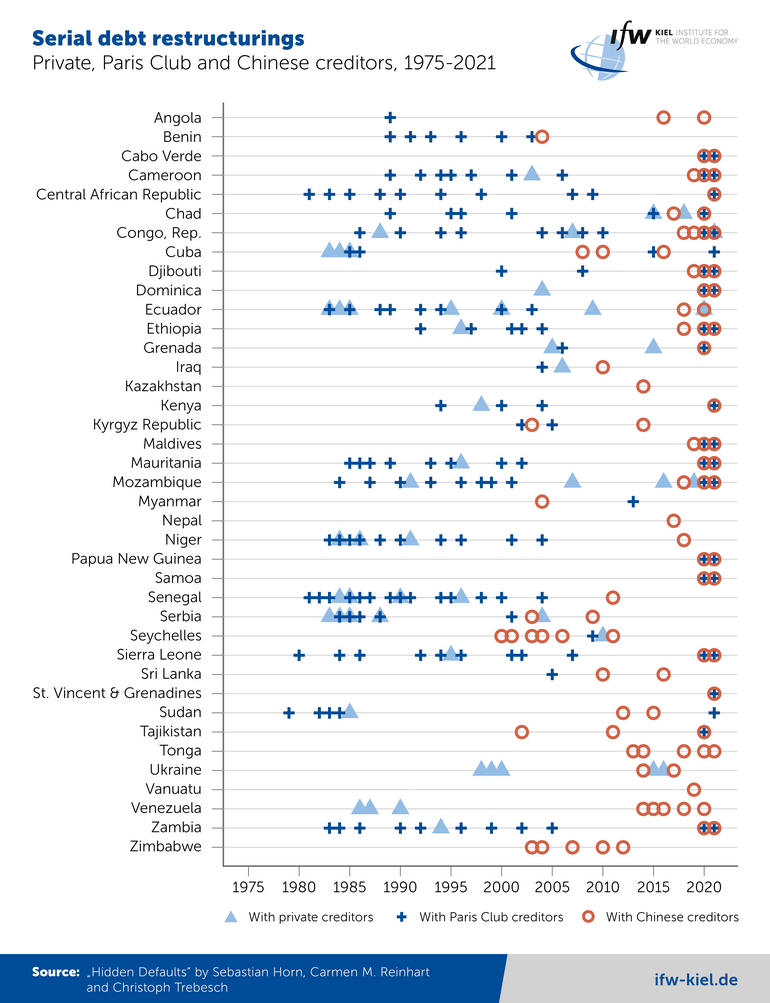

The authors show that China has become the central player in public debt lending and restructuring in developing countries. Since 2008, there have been 71 debt restructurings with Chinese creditors of 39 developing countries.

This is more than the number of restructurings with the so-called Paris Club, a grouping of the world's major creditor nations (68 restructurings), or with private creditors (21 restructurings of international bonds). African countries are frequently affected. They use China's loans to finance the expansion of their infrastructure, such as rail links, shipping ports, and airports.

"Payment problems and credit events vis-à-vis Chinese creditors are surprisingly frequent, especially considering that hardly anything is known about the events. Given the large size of the Chinese loans and the potential consequences of a debt overhang and default in developing countries, the lack of reporting by rating agencies is particularly puzzling," says Trebesch.

Many of the payment defaults are protracted. But the timing and size of the defaults are largely unknown, not least due to China's loan clauses, which often require confidentiality.

"We are likely to miss many defaults on Chinese debts, also because the very existence of the loan agreements is not publicly known. The hidden debt problem turns into a hidden default problem. This knowledge gap is a major challenge for debt sustainability and risk analyses of emerging and developing countries," Trebesch said.

The large scale of China's lending to developing countries and the contents of the Chinese loan contracts have been examined in two previous research papers involving the Kiel Institute (on the volume of loans "China’s international lending is much higher than previously known"; on the content of China's loan contracts: "New Study Shines a Light on Beijing’s Secretive International Lending Program").

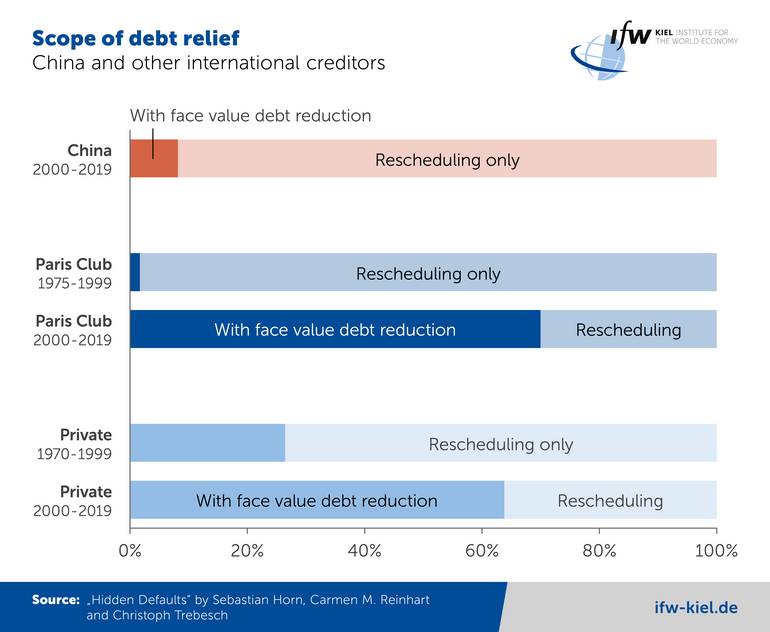

Although the data do not allow a comprehensive analysis of China's handling of defaults, they do show that significant debt relief is very rare. In the vast majority of payment problems, China's state-owned banks merely grant an extension of repayment periods, with otherwise unchanged loan terms. A reduction in interest rates has been granted in only 10 cases over the past 20 years, and a reduction in the nominal debt burden in only 4 cases.

"China’s current approach to crisis resolution resembles that of Western creditors in the 1980s and 1990s. But history has shown that debt overhang can only be resolved through deep debt relief, meaning a reduction of debt burdens and interest rates. Should Chinese lenders repeat the errors of previous eras, a decade of recurring payment problems and serial debt rescheduling on China’s loans may lie ahead," Trebesch said.