Foreign Capacity Utilization: An Indicator for the Exports of German Capital Goods

Capacity utilization is an important determinant of investment activity in the business sector. In general, an increase in capacity utilization leads to an increase in investment activity and thus to an increase in demand for capital goods. Likewise, an increase in foreign capacity utilization should lead to an increase in demand for domestic capital goods.

Capacity utilization is an important determinant of investment activity in the business sector. In general, an increase in capacity utilization leads to an increase in investment activity and thus to an increase in demand for capital goods. Likewise, an increase in foreign capacity utilization should lead to an increase in demand for domestic capital goods.

To analyze whether an increase in the foreign capacity utilization results in an increase in German capital goods exports, we calculated an indicator of foreign capacity utilization from the perspective of German exporters. The indicator is based on business surveys analyzing capacity utilization in the manufacturing sector in 37 countries that, together, bought more than 90 percent of German exports in 2011. The indicator is calculated by weighting the capacity utilization in each country by the share of German exports that it bought.

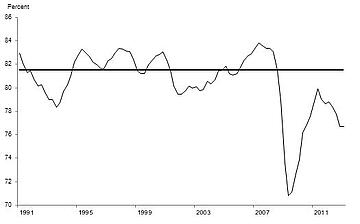

The resulting indicator shows the foreign capacity utilization from the perspective of German exporters (Figure 1). Capacity utilization fell markedly during the financial crisis in 2008 and 2009, reaching its historical low of about 71 percent in the second quarter of 2009. Though capacity utilization has recovered noticeably since the financial crisis, the long-run average of 81.5 percent has not been reached again. On the contrary, since the second quarter of 2011, capacity utilization has decreased again. One reason for this decrease has been the weak economic performance in euro area countries that have been suffering from a sovereign debt crisis.

Figure 1 – Capacity Utilization in the buyer countries 1991–2012

Source: National Sources; own calculations.

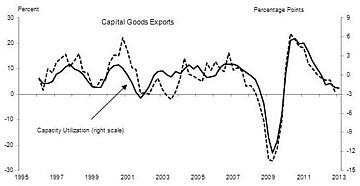

The correlation between capacity utilization and investment is strong both from a theoretical and an empirical point of view.1 Though this correlation has been found to obtain only at a national level so far, it should obtain at the international level as well, i.e. an increase in foreign capacity utilization should in general lead to an increase in foreign investment and thus in an increase in German capital goods exports.2 Indeed, foreign capacity utilization and German capital goods exports show a strong comovement, which was particularly pronounced during the recession of 2008 and 2009 and during the subsequent recovery (Figure 2).

Figure 2 – Foreign Capacity Utilization and German Capital Goods Exports

Sources: National sources via Thomson Financial Datastream; own calculations.

The correlation coefficient between foreign capacity and German capital goods exports (based on quarter-on-quarter growth rates) for the time period from 1995 to 2012 is 72 percent. Due to the fact that data for foreign capacity utilization is available roughly three months prior to the data for capital goods exports, our descriptive analysis suggests that the capacity utilization is a proper leading indicator.3

Comparison with other leading indicators

We evaluate the forecast accuracy of foreign capacity utilization not only against an autoregressive model (AR model), but also against two other leading indicators, i.e. the ifo export expectations for German companies and new orders from abroad published by the German Federal Bureau of Statistics.4 Though the focus is somewhat different for each of the three leading indicators, all of them are highly correlated with each other, whereby the foreign capacity utilization and the export expectations have the highest correlation, namely 85 percent (Table 1). However, the indicator for foreign capacity utilization correlates more strongly with German capital goods exports than export expectations or new orders.

Table 1 – Correlation between leading indicators and German capital goods exports

Formal comparison of forecast accuracy

In order to compare the forecast accuracy of the foreign capital utilization indicator for the German capital goods exports to the two other leading indicators, we perform an out-of-sample forecast comparison. To do so, we use quarterly data for the period from 1995 to 2011 to estimate forecasting models that explain the quarter-on-quarter growth rate of the capital goods exports by means of each indicator.5

To be more specific, we specify the models using a model selection procedure that successively eliminates each variable with a significance level smaller than 95 percent. We use an AR model as a reference model to evaluate the forecast accuracy and perform an out-of-sample forecast comparison for the period from 2005 to 2011.6 For a forecast in period t, we estimate each model only up to period t-1 to account for parameter uncertainty.

We also take the temporal availability of the indicators into account. Foreign capacity utilization data are available already at the beginning of the second month in a quarter—at least for the industrial countries. Export expectations data are available at the end of the third month in a quarter for the respective quarter and the data for the new orders from abroad are published at about the same time as the data for the capital goods exports, namely six weeks after the end of a quarter. Therefore, for the forecast of the capital goods exports in quarter t, we assume that foreign capacity utilization is available for this quarter (t), that export expectations are available for the first month of the quarter t, and that the new orders from abroad are available for the quarter t-1. Since the data we have for the export expectations pertains only to the first month, we use the value of the first month to forecast the quarterly value, whereby we only include lagged values for new orders from abroad.

Table 2 – Forecast accuracy of the indicators

To measure the quality of the forecasting accuracy of the models, we use the mean absolute error and the root mean squared error (MAE and RMSE). Then we divide the forecast errors of the three indicators by the forecast errors of the AR model. Thus, a value of the MAE or RMSE smaller than one indicates that the respective indicator exhibits higher forecast accuracy than the AR model. The forecast errors show that each of the three indicators exhibits higher forecast accuracy than the AR model (Table 2). The model based on the capacity utilization exhibits the smallest forecast errors. The model based on the export expectations exhibits slightly higher forecast errors, and the model based on the incoming orders exhibits the highest forecast errors.

Further, we test whether the forecast accuracy of the models differ significantly from each other. The Diebold-Mariano test shows that the model based on the foreign capacity utilization produces significantly smaller forecast errors at the 5 percent level than the AR model, and the model based on export expectations produces significantly smaller forecast errors at the 15percent level than the AR model. We also test for the predictive accuracy between the indicators. This test shows that the forecast errors of the model based on the foreign capacity utilization are significantly smaller at the 10percent level than the forecast errors of the model based on new orders from abroad, and are significantly smaller at the 15 percent level than the forecast errors of the model based on export expectations.

Conclusion

As expected from a theoretical and empirical point of view, we provide evidence for a positive correlation between the foreign capacity utilization and German capital goods exports. We show that the indicators foreign capacity utilization, export expectations, and new orders from abroad are all useful for forecasting German capital goods exports. However, models based on foreign capacity utilization exhibit a higher forecast accuracy than models based on the other two indicators that are frequently used. One advantage of using foreign capacity utilization as an indicator for German capital goods exports is that data for this indicator are available prior to the data for other indicators. Overall, this indicator is a valuable complement to the set of indicators available for forecasting German exports.

_____________________

1See, e.g., Jorgenson and Siebert (1968), Blanchard et al. (1993), or Shapiro (1989).

2When forecasting the business cycle, one often is interested in the real development of a variable. Therefore, we adjust the time series for capital goods exports by the export prices for German capital goods.

3Foreign capacity utilization in a quarter can be determined at the beginning of the second month of the quarter.

4Since the correlation between the capital goods exports and the export expectations of all companies is stronger than the correlation between the capital goods exports and the export expectations of companies only dealing with capital goods, the export expectations of all companies are included in the analysis. For the same reason, aggregate new orders from abroad are included in the analysis rather than new orders of capital goods from abroad.

5The analysis is based on quarterly data, because most of the countries collect the capacity utilization data only once in a quarter. An analysis based on quarterly data is appropriate anyway, because of high volatility in monthly data.

6This is a very short time period for an out-of-sample comparison. Nonetheless, it is not possible to prolong this period given the available data.

References

- Blanchard, Olivier, Changyong Rhee, and Lawrence Summers (1993). The Stock Market, Profit, and Investment. The Quarterly Journal of Economics 108 (1): 115–136.

- Diebold, Francis X., and Roberto S. Mariano (2002). Comparing Predictive Accuracy. Journal of Business & Economic Statistics 20 (1): 134–144.

- Jorgenson, Dale W., and Calvin D. Siebert (1968). A Comparison of Alternative Theories of Corporate Investment Behavior. The American Economic Review 58 (4): 681–712.

- Shapiro, Matthew D. (1989). Assessing the Federal Reserve’s Measures of Capacity and Utilization. Brooking Papers on Economic Activity 20 (1): 181–241.

(English Version of an article in Wirtschaftsdienst 12/20012: http://www.wirtschaftsdienst.eu/archiv/jahr/2012/12/; for an updated version of the capacity utilization indicator see: http://www.ifw-kiel.de/think-tank/macroeconomic-forecasts/indikatoren/indicators-for-german-exports.