News

Coronabonds: EU community bonds are a proven crisis instrument

© European Union 2019 - Source : EP

"History shows that, in deep crises, European governments have always been prepared to issue community bonds and to be liable for them. The institutions required for this were developed flexibly and at short notice. The EU should now use this proven and effective instrument to support countries like Italy in coping with the consequences of the corona pandemic," said Kiel Institute Head of Research Christoph Trebesch. Together with Sebastian Horn and Josefin Meyer from the Kiel Institute, he analysed the historical development of European crisis instruments.

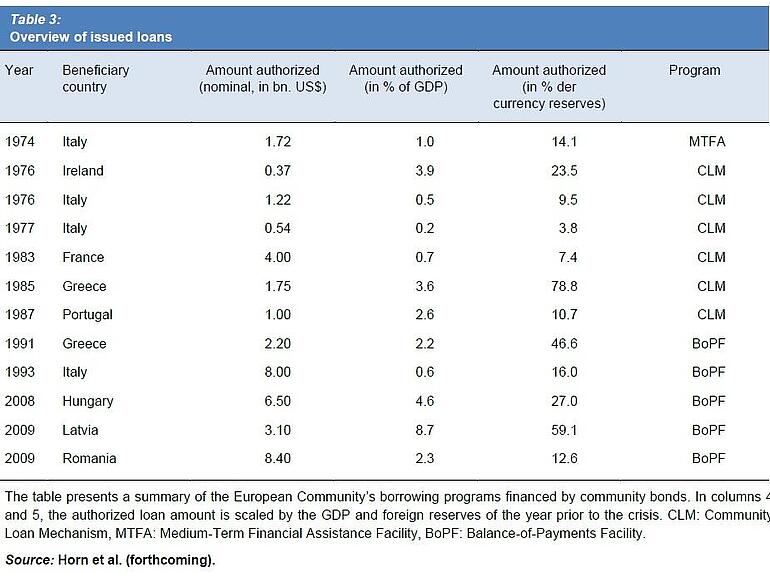

The first joint bond was issued in 1976 in favor of Italy and Ireland to counter the economic shock of the oil crisis. Italy was particularly hard hit and slid into a deep recession, with GDP shrinking by

-2% in 1975. In addition to European loans to Italy, Germany also showed bilateral solidarity and in 1974 granted an intergovernmental billion-euro loan to Rome.

In the 1980s and 1990s further European loans followed for France, Greece, and Portugal, and, after 2008, for Hungary, Latvia, and Romania. In addition, the ESM for eurozone countries was established in 2012.

In total, the European Community has so far raised 38.8 billion US Dollars in loans via community bonds in nominal terms, not adjusted for inflation, and distributed them to crisis countries. This figure does not include the loans from the EFSF and ESM. "The aid loans were in some cases very high, at over 5 percent of the GDP of the recipient countries, and all European community bonds have been repaid in full and on time," said Trebesch.

The way for Community Bonds was paved in 1975 with the so-called Community Loan Mechanism (CLM), which was supported by the German Chancellor Helmut Schmidt, among others. The aim was to raise European community bonds via the private capital market in order to support countries in crisis. In 1981, the instrument was reformed to form the so-called Balance of Payment Facility.

The Community bonds were guaranteed primarily through the EU budget. In addition, there were guarantee obligations on the part of the member states. If a crisis country failed to meet its obligations to the community, the other member states guaranteed debt service according to fixed quotas, whereby Germany assumed a guarantee of 22.02%.

Trebesch: "In the debate on European crisis rescue, it is often claimed that corona bonds, i.e. common European debts, would breach a taboo. However, a look back shows that this is not true. Since the 1970s, European community bonds have been repeatedly issued and successfully used to overcome financial and economic crises in Europe.”