News

China’s international lending is much higher than previously known

Renminbi © faungg's photos_CC BY-ND 2.0

The Kiel Working Paper No. 2132 "China's Overseas Lending" provides the first comprehensive picture of China’s overseas lending and other financial flows. The researchers Sebastian Horn (University of Munich, Kiel Institute), Carmen Reinhart (Harvard University), and Christoph Trebesch (Kiel Institute) compiled data from over six decades from numerous public and non-public sources. The data covers thousands of loans and grants to 152 countries and resulting obligations.

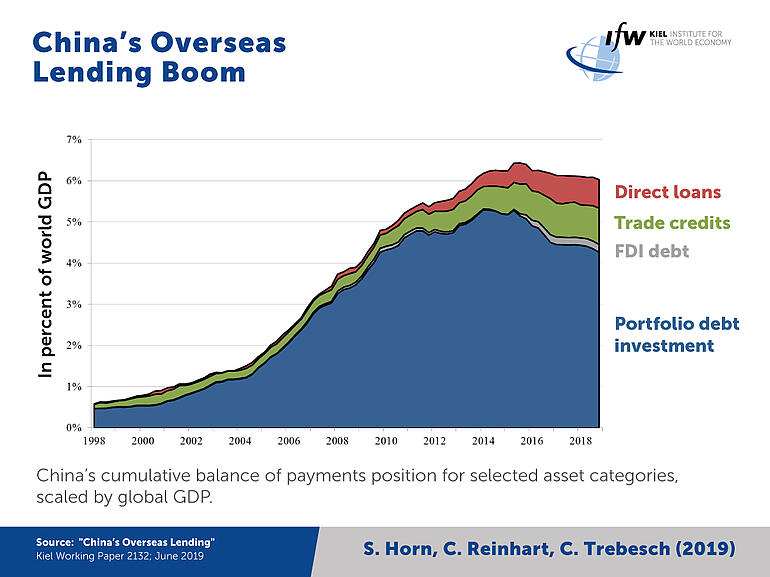

Between 2000 and 2017, the obligations of foreign debtors to China increased from less than 500 billion USD to more than 5 trillion USD—or from around one percent of global economic output to more than six percent. The majority of debt claims has been acquired in international bond markets by China’s state-owned central bank. China’s foreign portfolio debt holdings have strongly increased since the early 2000s. In addition, China’s government has extended increasing sums of direct loans, in particular to developing and emerging countries.

Chinese state banks have granted around a quarter of total bank lending to emerging markets. China has thus become the world's largest official creditor, easily surpassing the International Monetary Fund (IMF) or the World Bank. When adding direct investments and equity flows, China’s total capital stock abroad now exceeds 8 percent of world GDP.

Around 50 percent of China's international lending to developing and emerging countries is not included in official statistics. They are not recorded by multilateral surveillance institutions such as the IMF or the Paris Club, by rating agencies, nor by private data providers.

"China has always been an active international creditor, lending large amounts to Communist brother states during the cold war era. But the increase in total credit outflows over the past two decades has been almost unprecedented, comparable only to the waves of US official lending in the wake of World War 1 and 2. China’s international lending boom is primarily a result of the country’s rapid economic growth, but also due to the “going global” policy of the Chinese state," says Christoph Trebesch, head of the Research Area International Finance and Global Governance at the Kiel Institute for the World Economy.

For the 50 top recipients of Chinese loans—mainly smaller or poorer countries—debt to China grew from around one percent of their GDP in 2005 to over 15 percent of GDP n 2016. For these countries, loans from China account for 40 percent of their total external debt, on average.

"What makes China's international lending unique is not only its sheer size and the lack of transparency, but also the fact that it is almost entirely state-driven, by the government, China’s state owned banks or by the state-controlled central bank," says Trebesch. At the same time, China often lends at market interest rates, with risk premia, and partly with collateral clauses that secure repayment in kind, e.g. in the form of oil exports.

Many of the projects financed by China can be benefical for recipients, in particular in infrastructure. The magnitude and opaqueness of China’s lending, however, poses a challenge for debtor countries and international financial markets. Private investors or the IMF can hardly assess the debt sustainability and crisis probability of countries, if a considerable portion of foreign debt (to China) is simply unknown. Country risk analysis is left in the dark.

"The combination of opaqueness and a comparatively high degree of seniority entails significant risks in the event of financial crises. An internationally coordinated response and fair burden sharing among all creditors becomes more difficult to organize," says Trebesch.

Germany, too, is heavily indebted to China’s central bank. China holds around 370 billion USD of German Bunds, according to the author’s estimates. This amounts to 10 percent of German GDP. For the euro zone as a whole, China holds 850 billion USD of bonds, which corresponds to 7 percent of euro area GDP.